Yield Curve Flattening as Oil Crisis Reshapes Bond Markets

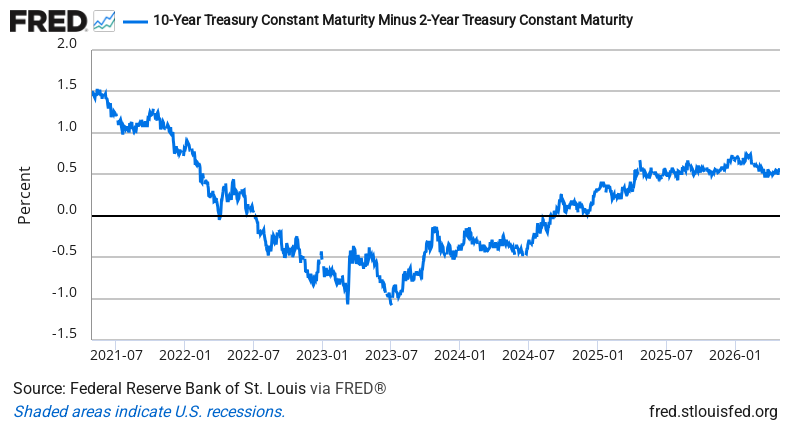

The spread between 10-year and 2-year Treasury yields compressed to 0.52% Monday from 0.57% Friday — a 5 basis point flattening that reflects how the Strait of Hormuz crisis is reshaping Fed expectations. While we’re still well clear of inversion territory, this compression suggests bond traders are pricing in a higher-for-longer rate environment as oil holds near $95.

The flattening comes as markets recalibrate around a Fed that’s paused rate cuts indefinitely due to energy-driven inflation risks. Before the Strait closure in February, the Fed was eyeing potential easing with core inflation settling around 2.5%. Now, with every sustained $10 oil premium adding roughly 0.6% to CPI, traders are betting short-term rates stay elevated while long-term growth expectations moderate. That’s classic curve flattening dynamics — and it’s happening faster than many expected.

What makes this move notable is the speed. The 8.8% daily compression follows several sessions of volatility as markets digest the reality of prolonged energy disruption. Historically, when geopolitical crises create sustained inflationary pressure, yield curves flatten as the Fed prioritizes price stability over growth. The 1990 Gulf War and 1979 Iran hostage crisis both triggered similar patterns — though neither involved a complete Strait closure like we’re seeing now.

Many professional investors view curve flattening environments as rotation catalysts — away from rate-sensitive sectors like utilities and REITs toward companies that can pass through higher costs. Energy exporters and companies with pricing power typically outperform, while margin-compressed importers lag. The current risk-on sector rotation (tech up 10.3% vs SPY this month) suggests investors are already positioning for this playbook.

Bottom Line: This isn’t your typical curve flattening driven by recession fears — it’s energy-induced policy constraint flattening. The question isn’t whether we’ll see inversion, but whether the Fed can thread the needle between containing energy inflation and avoiding growth damage.

Source: Federal Reserve Economic Data (FRED)

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free