Inflation’s Surprise Retreat Is the Fed’s Permission Slip

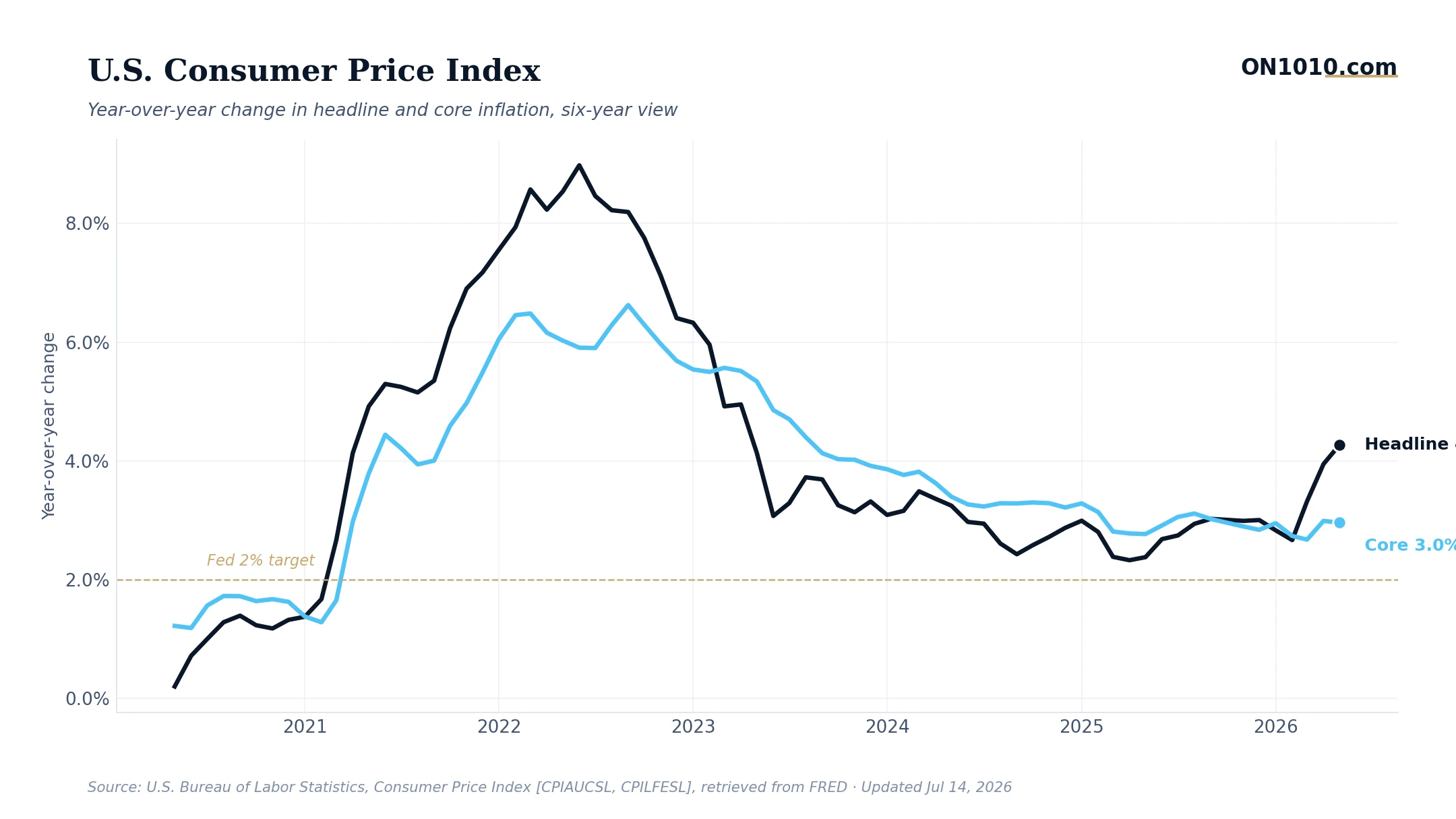

According to CNBC, the Consumer Price Index rose 3.5% annually in June, coming in below the 3.8% consensus forecast as easing energy prices did a lot of the heavy lifting. The headline number is easy to wave off as a modest beat. Don’t.

A 0.3 percentage point miss against expectations sounds small, but in the current policy environment it shifts the conversation meaningfully. The Fed has been threading a needle between keeping rates high enough to finish the inflation job and not holding them there so long that it cracks the labor market or business investment. A softer CPI print gives policymakers more breathing room, and more importantly, it changes what markets expect them to do next.

Energy prices driving the disinflation is a double-edged story. On one hand, it’s the most volatile component of CPI, which means the cooling could reverse quickly if supply dynamics shift. On the other hand, lower energy costs are essentially a margin gift to every business that moves goods or runs facilities, which covers most of the economy. When input costs fall and companies hold pricing, margins expand. And as the analytical framework here has always argued, expanding margins are a leading indicator of more hiring and more investment down the road.

The sector rotation data today reinforces that the market is reading this constructively. Financials are running nearly 4.2 percentage points ahead of SPY, and Industrials are outperforming by 3.0 points. That’s not a defensive posture. Historically, when CPI surprises to the downside in a late-cycle environment, investors have leaned into rate-sensitive and capital-intensive sectors, anticipating that the cost of borrowing for expansion gets cheaper before the economy actually slows.

The question worth sitting with: is this one month of good luck on energy, or the beginning of a broader disinflation trend that gives the Fed room to ease? That answer matters enormously for how capital gets allocated over the next 12 months.

Bottom Line: Inflation coming in below expectations is unambiguously good news for margins, and the market’s sector rotation today suggests institutional money is already thinking about what cheaper credit does to business investment.

Read more: CNBC Economy

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free