Long-Term Inflation Expectations Edge Higher as Markets Parse Energy Shock

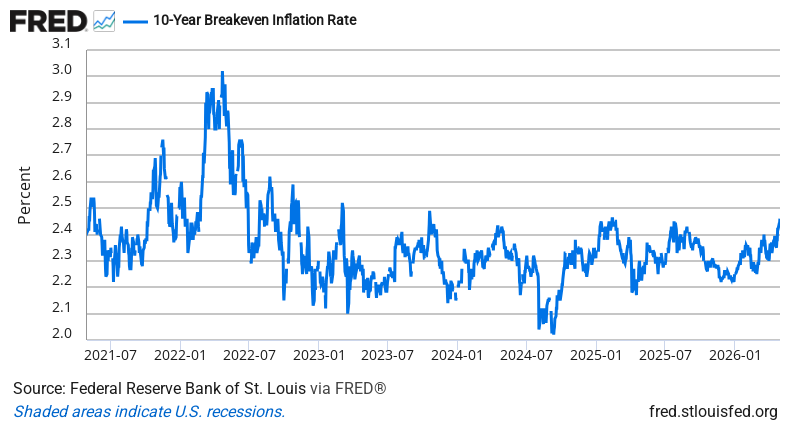

The 10-year breakeven inflation rate ticked up to 2.46% yesterday, its highest level in a week and continuing a gradual climb from 2.38% just five trading days ago. That’s still well within the Fed’s comfort zone, but the steady upward drift tells a story about how bond markets are pricing in the persistent effects of the Strait of Hormuz crisis.

Here’s what’s interesting: breakeven rates are rising, but slowly. Despite oil spiking from $66 to $95 since the Strait closure in February, long-term inflation expectations have only moved about 8 basis points higher over the past week. That suggests investors still view the energy shock as temporary rather than structural. But the consistent daily increases indicate growing concern that higher energy costs could prove stickier than initially hoped, especially with Iran’s new leadership vowing to keep the Strait closed.

This measured response reflects a market trying to balance two forces. Yes, every sustained 10% oil premium historically adds about 0.6% to near-term CPI readings. But the US is a net energy exporter, meaning higher prices benefit domestic producers even as consumers pay more. The real question is whether this energy shock fundamentally changes the disinflationary trend that had CPI and PCE settling around 2.5% before February.

Many professional investors view breakeven rates between 2.3-2.7% as a sweet spot where the Fed doesn’t need to panic but stays alert. In this type of environment, portfolios often benefit from a mix of energy exposure (which profits from higher prices) and Treasury Inflation-Protected Securities (TIPS), which adjust with actual inflation. Energy-intensive sectors face margin pressure, while companies with pricing power tend to outperform.

Bottom Line: The bond market isn’t panicking about long-term inflation, but it’s no longer betting on a quick return to pre-crisis levels either. The question investors should be asking: is this gradual repricing of inflation risk the calm before a bigger storm, or a sign that markets are adapting to a new normal?

Source: Federal Reserve Economic Data (FRED)

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free