Fed Pivots From Energy Crisis to Growth Questions as Markets Signal New Phase

The Opening Bell

The bond market is quietly telling us the energy crisis chapter is ending, and asking what comes next. With Treasury yields backing off recent peaks and the yield curve continuing to normalize, investors are shifting focus from oil shocks to whether this productivity-driven growth cycle has legs. Today’s employment data could provide the first real answer.

Market Snapshot

Fed Funds Target Range: 3.5%-3.75%

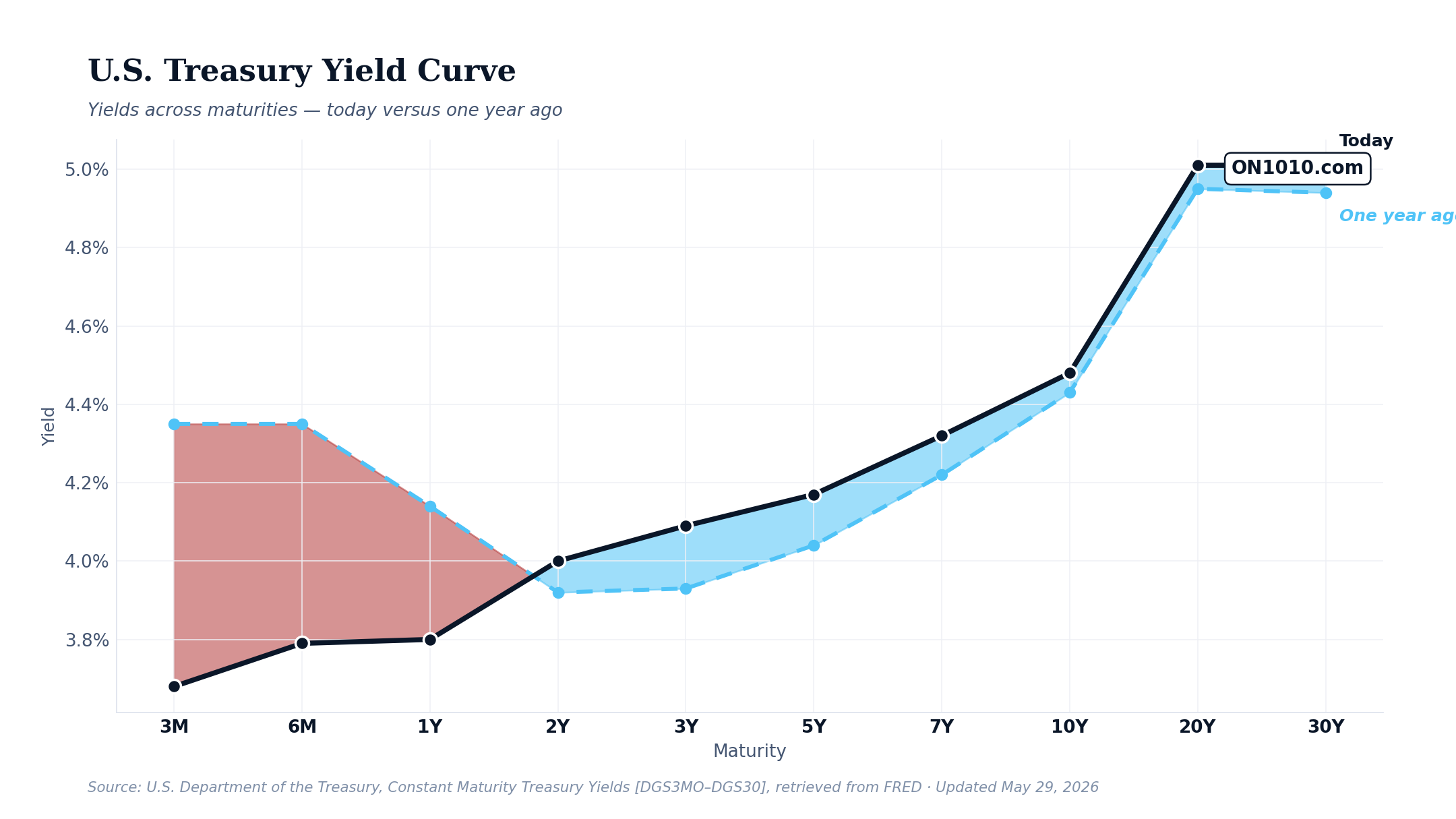

10-Year Treasury: 4.48%

2-Year Treasury: 4.0%

10Y-2Y Spread: 0.46% (normal)

Breakeven Inflation (10Y): 2.39%

The yield curve continues its steady march toward normal, with the 10Y-2Y spread now at its widest point in weeks. More telling: inflation expectations are holding steady despite ongoing energy volatility, suggesting the market believes the worst of the oil shock pricing is behind us.

What Moved Yesterday

Corporate America’s productivity story took center stage as after-tax profits surged 3.3% to nearly $3.92 trillion. But here’s what matters for the growth outlook: companies are achieving these record margins through efficiency gains, not pricing power. That’s sustainable margin expansion, the kind that funds more investment and hiring rather than just enriching shareholders.

The jobs data painted a more nuanced picture. Initial claims jumped to 215,000, hitting three-week highs, while the underlying employment trends show companies being selective rather than desperate. This isn’t weakness, it’s normalization. After months of energy-crisis hiring freezes, businesses are returning to normal talent evaluation processes.

Housing markets delivered the clearest signal that higher rates are working as intended. Mortgage rates climbing to 6.53% are doing exactly what the Fed hoped: cooling demand without crashing the market. The 63% plunge in oil inventories suggests supply chains are finally rebalancing after months of Strait of Hormuz disruptions.

Today’s Playbook

All eyes turn to the employment situation report, where the market expects payroll growth around 180,000. But the real story will be in wage growth and labor force participation. If wages are rising faster than productivity gains, that signals inflation pressure ahead. If they’re tracking productivity, around 2.5-3% annually, that’s the goldilocks scenario.

Watch for any Fed speakers addressing the shift from crisis management to growth policy. With energy prices stabilizing and inflation expectations anchored, the central bank faces a new question: should monetary policy support this productivity boom or lean against potential asset bubbles?

The bond market’s recent pullback from 4.67% peaks suggests traders are positioning for a different 2026 than they expected six weeks ago. A strong jobs number that shows sustainable wage growth could cement the “productivity boom” narrative. A weak number might revive recession fears that have been dormant since the energy crisis began.

The Bigger Picture

We’re witnessing something that hasn’t happened since the late 1990s: corporate profit growth driven by genuine productivity gains rather than cost-cutting or pricing power. The combination of record margins and stable inflation expectations suggests the economy has successfully absorbed the energy shock while maintaining its underlying growth trajectory.

This mirrors the mid-1990s pattern when technology-driven productivity gains allowed the economy to grow faster than traditional models predicted without triggering inflation. The difference now: this productivity boom is happening against a backdrop of normalized monetary policy, not the zero-rate environment of the post-2008 era.

Bottom Line: The market is pricing in a post-crisis economy where growth comes from doing more with less, not from emergency stimulus. If today’s jobs data confirms that productivity gains are translating into sustainable wage growth, we’re looking at a fundamentally different growth cycle than anything we’ve seen in two decades.

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free