The Morning Bell: Bond Market Breaks From Energy Narrative as Real Growth Questions Surface

THE OPENING BELL

Forget oil for a moment. The bond market is quietly telling a different story this morning, one that has nothing to do with the Strait of Hormuz and everything to do with whether the economy can actually grow without artificial support. While crude trades near $88 and everyone debates energy shocks, Treasury yields are drifting lower and the curve is steepening in a way that suggests investors are starting to price in something more fundamental: a growth slowdown that productivity gains might not be able to mask forever.

MARKET SNAPSHOT

Fed Funds Target Range: 3.5%-3.75%

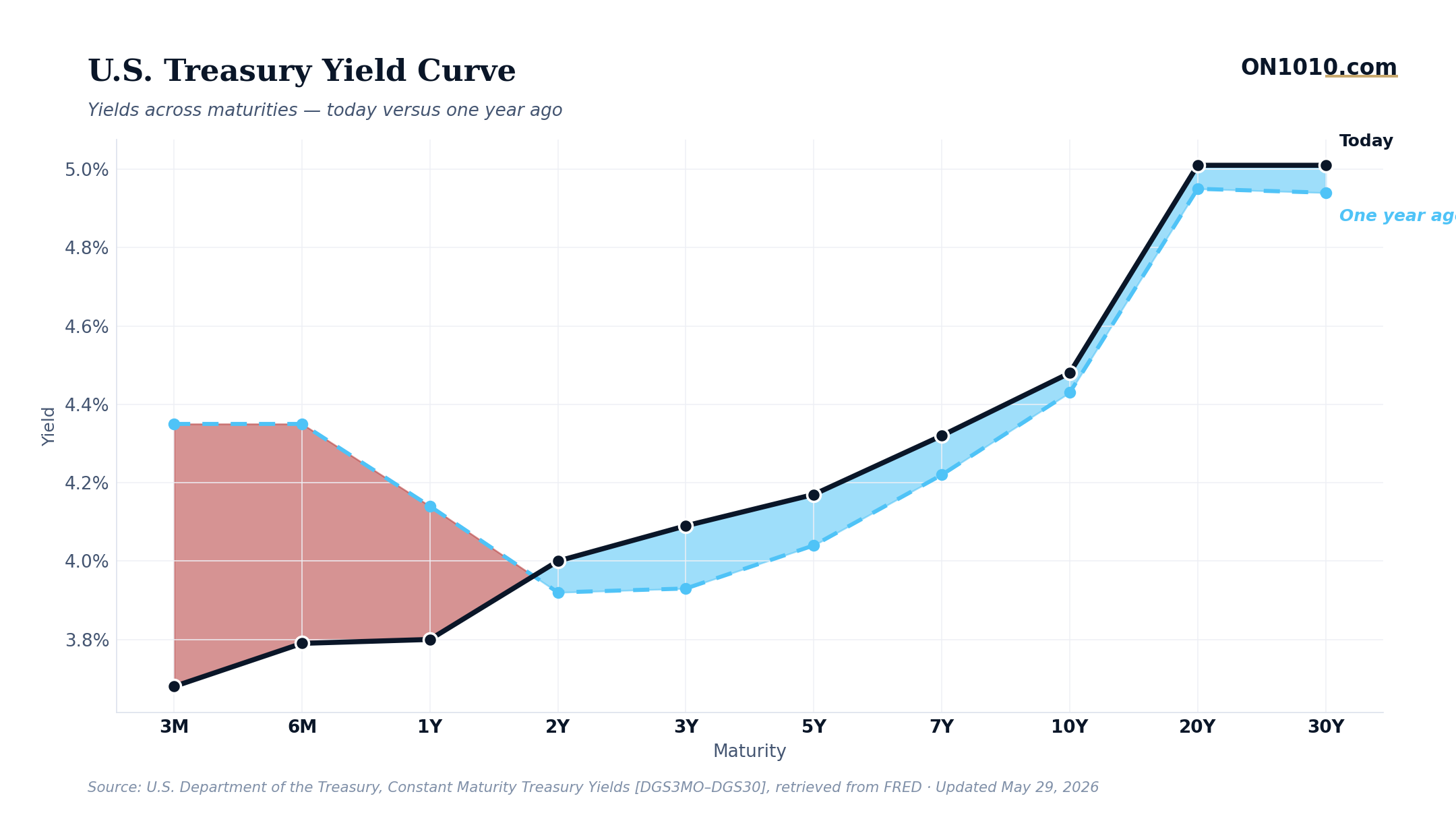

10-Year Treasury: 4.48%

2-Year Treasury: 4.0%

10Y-2Y Spread: 0.46% (normal)

Breakeven Inflation (10Y): 2.39%

The yield curve’s quiet steepening to 46 basis points tells a more nuanced story than the headline numbers suggest. Ten-year yields have dropped 19 basis points from last week’s peak while inflation expectations hold steady at 2.39%. That’s not energy fear driving bonds higher, it’s growth doubt.

WHAT MOVED YESTERDAY

The most important data point wasn’t about oil. Corporate profits surged to a record $3.92 trillion, powered by what looks like a genuine productivity boom that’s allowing companies to expand margins even as they face energy headwinds. But here’s the twist: jobless claims jumped to 215,000, the highest in three weeks, while mortgage rates climbed to 6.53% for the fourth straight week.

That combination matters more than most realize. Corporate America is demonstrating it can generate profits through efficiency rather than just volume growth. But the labor market is showing the first signs of that efficiency translating into something workers won’t like: fewer jobs needed to generate the same output. When productivity surges, employment growth typically lags by 6-12 months. We might be entering that phase now.

The housing data reinforces the broader theme. Mortgage rates above 6.5% aren’t just a number, they’re a threshold that historically separates normal housing markets from distressed ones. Add in the fact that natural gas jumped 9% this week as summer demand kicks in early, and you have an economy that’s being squeezed from multiple directions even as corporate profits hit records.

TODAY’S PLAYBOOK

Watch how markets react to any housing-related data or commentary today. With mortgage rates at 6.53% and climbing, the housing sector is approaching a potential inflection point that could ripple through the broader economy. Housing drives everything from construction jobs to furniture sales to local government revenues. When it stalls, the effects cascade.

More importantly, pay attention to any Fed commentary that touches on the productivity-employment tradeoff. If companies can maintain profit growth while hiring fewer workers, the traditional relationship between low unemployment and wage inflation breaks down. That could give the Fed more room to cut rates later this year, but it also means the labor market might weaken faster than most expect.

Bond markets seem to be pricing in this possibility. The fact that 10-year yields are falling even as oil stays elevated suggests investors are betting on slower growth rather than persistent inflation. That’s a significant shift from the energy-driven narrative that’s dominated for weeks.

THE BIGGER PICTURE

We’re witnessing something that looks a lot like the mid-1990s productivity boom, when technology advances allowed companies to grow profits without proportional increases in employment. The difference is that this productivity surge is happening during an energy crisis, creating a unique set of economic pressures that don’t fit historical patterns perfectly.

The bond market’s behavior suggests investors are starting to focus on the second-order effects of this productivity boom. Yes, corporate profits are surging. But if companies can generate record earnings with fewer workers, what happens to consumer spending? What happens to the tax base that funds government spending? The productivity narrative has a dark side that markets are just beginning to price in.

Bottom Line: The economy’s productivity surge is creating winners and losers in ways that traditional models don’t capture. Corporate America is thriving, but the broader growth picture is more fragile than the profit numbers suggest. Bond markets are pricing this in ahead of the data.

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free