Bond Markets Flash Warning Signs as Inflation Prints Loom

The Opening Bell

Bond traders are quietly repositioning ahead of this week’s inflation data, with 2-year yields drifting lower even as energy prices hold near crisis highs. The shift suggests markets are pricing in a more complex Fed calculus than the simple “higher oil equals higher rates” narrative that dominated March. With eurozone inflation hitting 3.2% and fresh tariff noise from the Trump administration, the question isn’t whether inflation is accelerating but whether the Fed has room to maneuver.

Market Snapshot

Fed Funds Target Range: 3.75%

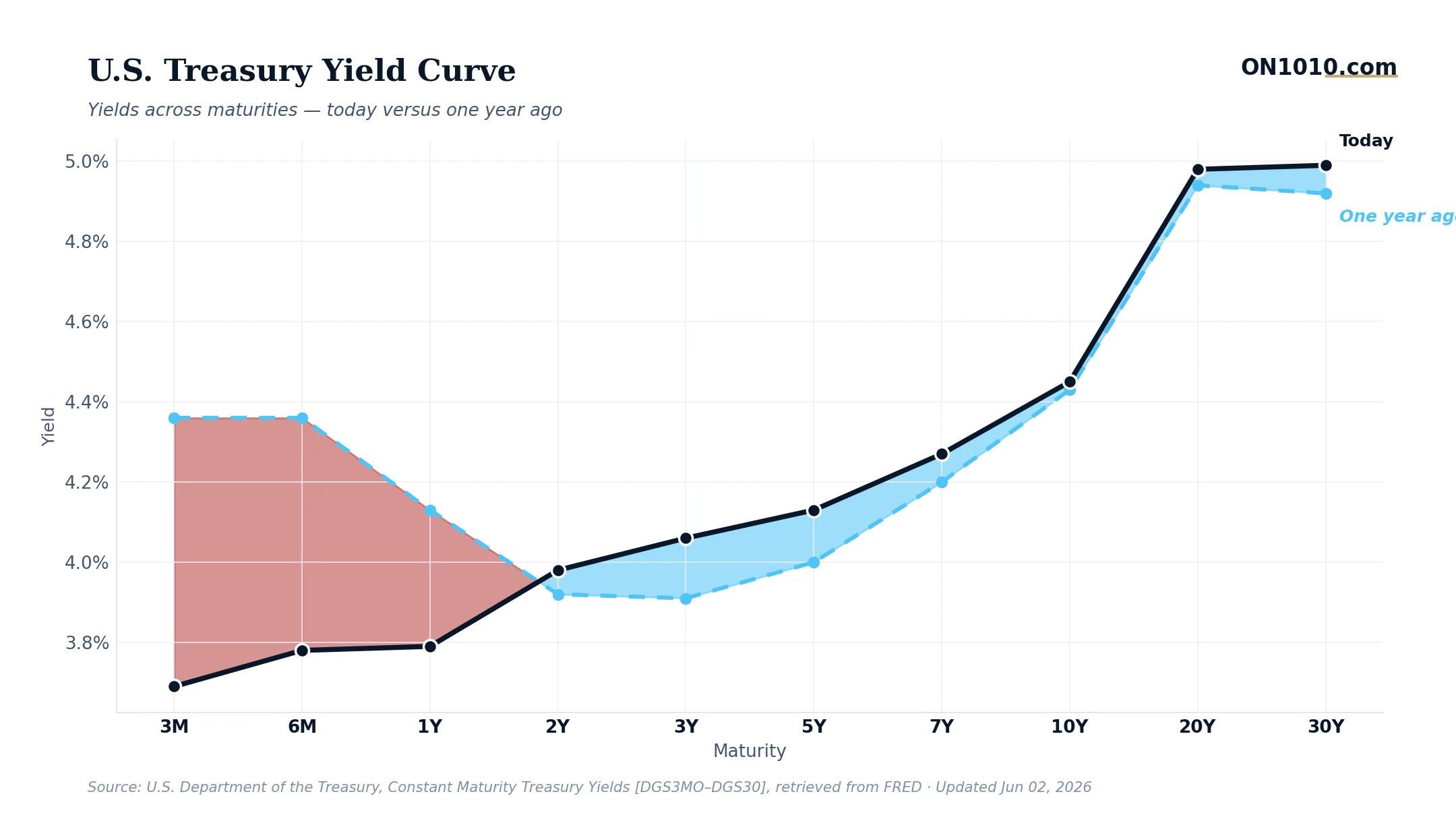

10-Year Treasury: Current data was unavailable at time of writing

2-Year Treasury: 3.98%

10Y-2Y Spread: Current data was unavailable at time of writing

Breakeven Inflation (10Y): Current data was unavailable at time of writing

The 2-year Treasury’s slide to 3.98% from 4.13% a week ago signals bond traders are backing away from their most aggressive Fed hawkishness bets. That 15 basis point drop suggests markets are beginning to question whether the central bank can actually follow through on implied rate hikes given mounting economic crosscurrents.

What Moved Yesterday

The eurozone’s 3.2% inflation print offered an uncomfortable preview of what’s coming stateside. Energy-driven price pressures are no longer confined to the pump as the Strait of Hormuz closure ripples through global supply chains. More telling: the Trump administration’s proposed 25% tariff on Brazilian goods signals trade policy is heating up again just as the Section 122 tariffs on China expire in July.

Amazon’s announcement of a four-day Prime Day event starting June 23 reveals corporate America’s inflation calculus. Retailers are extending promotional windows to capture consumer spending before back-to-school season hits strained household budgets. That’s classic late-cycle behavior when companies compete more aggressively for a shrinking pool of discretionary dollars.

Today’s Playbook

Markets are holding their breath for Thursday’s US CPI release, which could deliver the first 1-handle monthly print since the energy shock began. Every sustained 10% oil premium historically adds 0.6% to headline CPI, and with WTI crude trading at $90.91 (versus pre-crisis levels around $66), the arithmetic is straightforward. A hot print would force the Fed’s hand on rate policy just as economic growth signals turn mixed.

Watch for any commentary from Fed officials today about the interaction between energy-driven inflation and underlying price pressures. The central bank’s challenge: distinguishing between temporary energy shocks and persistent inflation expectations becoming unanchored. Bond markets are already pricing in this complexity, but equity investors may not be.

The Bigger Picture

We’re entering the most challenging phase of the energy crisis for monetary policy. The initial oil spike was absorbed by strategic reserve releases and consumer resilience. Now comes the harder part: secondary effects working through the broader economy as companies pass through higher input costs and consumers adjust spending patterns.

The parallel to 2008 is instructive, but not for the reasons most think. Then, oil spiked to $147 before the financial crisis hit. The key lesson: energy shocks don’t kill economies directly but they expose underlying vulnerabilities. Today’s vulnerability isn’t bank balance sheets but rather stretched corporate margins facing simultaneous pressures from energy costs, potential tariff escalations, and softening demand.

Bottom Line: Bond markets are pricing in Fed paralysis rather than Fed aggression. When 2-year yields fall while oil prices stay elevated, it signals traders think higher inflation will constrain growth more than it forces rate hikes.

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free