Yield Curve Quietly Steepening as Oil Shock Reshuffles the Deck

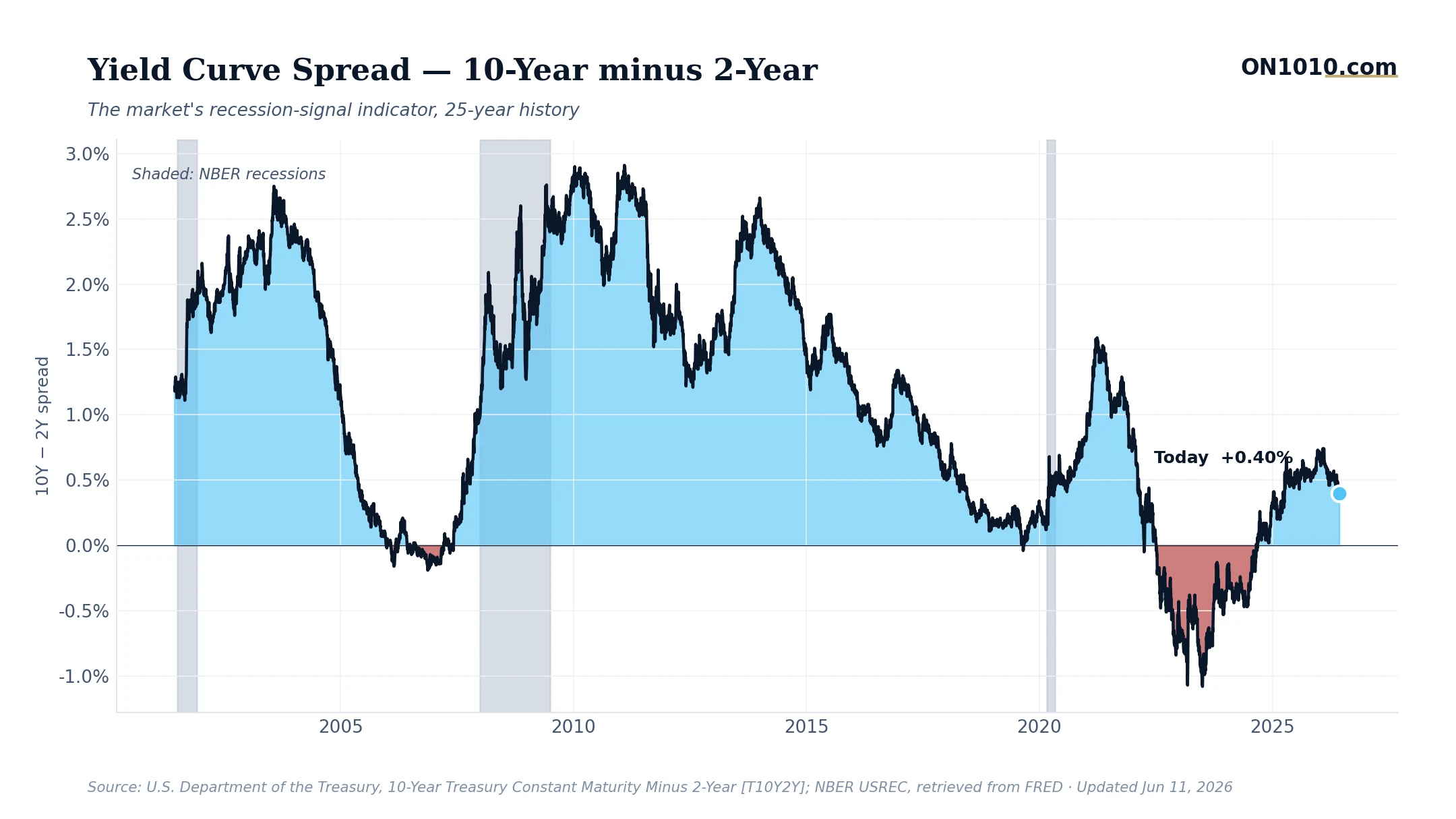

The 10-year/2-year Treasury spread ticked down to 0.4% yesterday from 0.42% the day before, a small move that masks a much bigger story. Six months ago, this curve was deeply inverted, flashing recession warnings. Today, it’s positive and has been quietly steepening since the Strait of Hormuz crisis began reshaping inflation expectations.

The mathematics of bond markets are working exactly as textbooks predict. With oil trading near $95 and monthly inflation prints threatening to show a 1-handle, long-term bonds are selling off harder than short-term ones. Investors are demanding higher compensation for the risk that today’s energy shock becomes tomorrow’s embedded inflation. Meanwhile, the Fed has shelved rate cuts, keeping the short end anchored. The result: a curve that’s steepening not because growth is accelerating, but because inflation uncertainty is rising.

This isn’t your typical expansion-driven steepening. In normal times, a steepening curve signals optimism, banks can borrow short and lend long profitably, credit flows, growth accelerates. But when steepening is driven by inflation fears rather than growth prospects, it creates a different dynamic. Real yields (after inflation) may actually be falling even as nominal yields rise, which historically has meant different outcomes for different asset classes.

Historically, inflation-driven steepening has favored real assets and energy producers while pressuring long-duration growth stocks and real estate. The current environment, with defensive sectors outperforming offensive ones by 3.4 percentage points over the past month, suggests markets are already positioning for this regime.

Bottom Line: The yield curve is un-inverting for the wrong reasons. It’s not signaling economic acceleration, it’s pricing in the risk that an energy crisis becomes an inflation problem.

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free