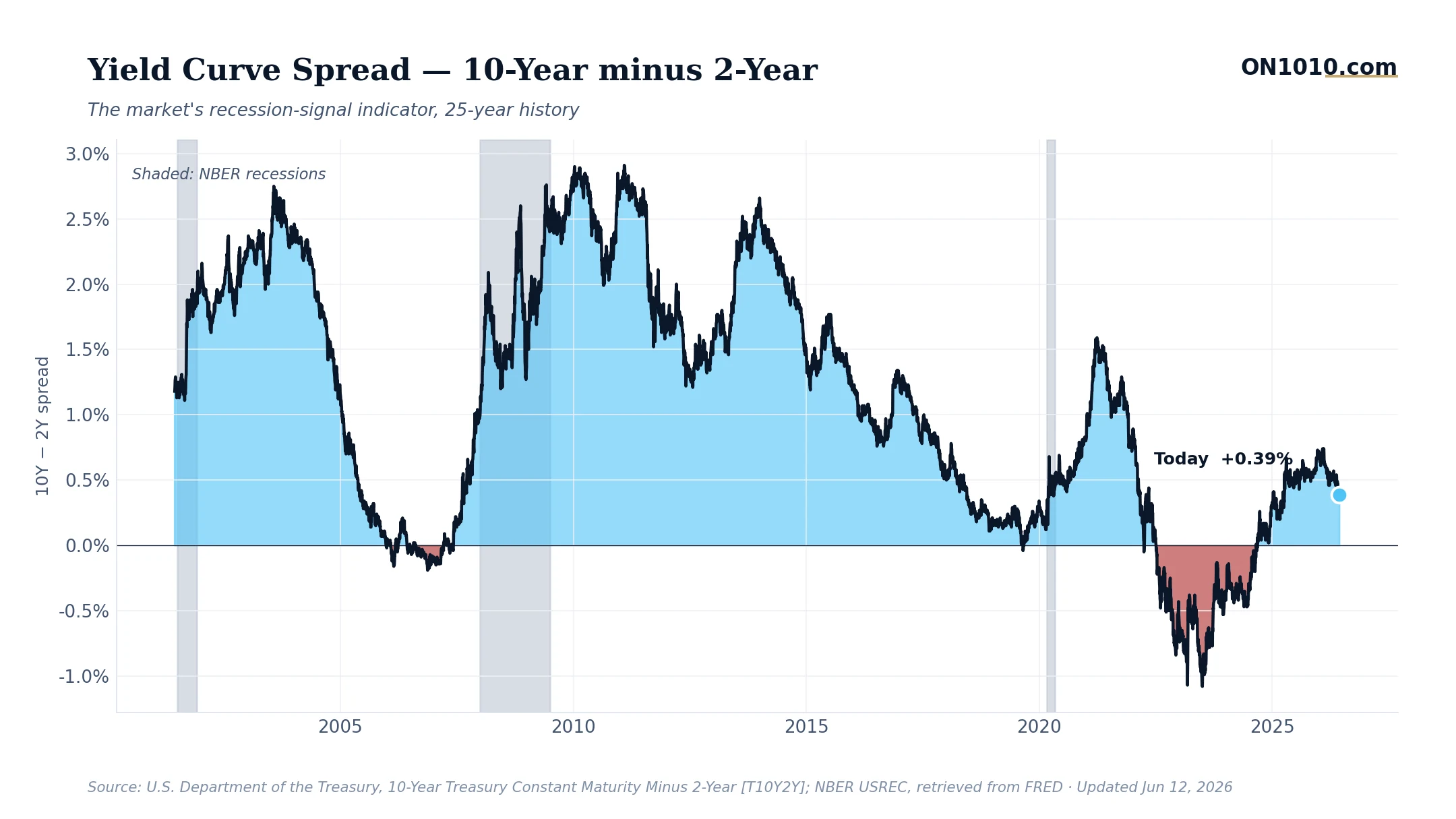

Treasury Curve Steepens Slightly, But Still Historically Flat

The yield curve is doing its impression of walking a tightrope. The 10-year minus 2-year Treasury spread ticked down to 0.39% from 0.40% yesterday, a narrow normal curve that’s been hovering around 40 basis points for the past week.

Here’s what makes this reading interesting: we’re sitting in an unusual sweet spot. The curve is technically positive (no recession alarm bells), but it’s flatter than normal historical periods when the economy was genuinely expanding. During the 2010s recovery, this spread averaged closer to 100-150 basis points. Today’s 39 basis points suggests bond markets see limited room for long-term growth acceleration, even with the economy avoiding immediate recession risks.

The flatness also reflects the Fed’s pause on rate cuts due to energy-driven inflation concerns. Short rates are staying elevated while long rates aren’t climbing much higher, a sign that bond investors expect any inflation spike from the oil shock to be temporary rather than persistent. Markets are essentially betting the Fed can contain price pressures without crushing growth.

Historically, this type of persistently flat curve, positive but compressed, has preceded periods where growth disappointed relative to expectations. In past cycles, investors have watched for either a meaningful steepening (growth acceleration) or inversion (recession warning). The in-between zone we’re in now often meant muddle-through economics: growth, but not much of it.

Bottom Line: A 39 basis point curve isn’t screaming danger, but it’s whispering caution about how much economic acceleration is really possible from here.

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free