China Just Surprised Everyone. Here Is What the Factory Data Actually Means for U.S. Growth.

The consensus heading into the second half of 2026 was that global demand would stay soft. China’s June factory data just complicated that story.

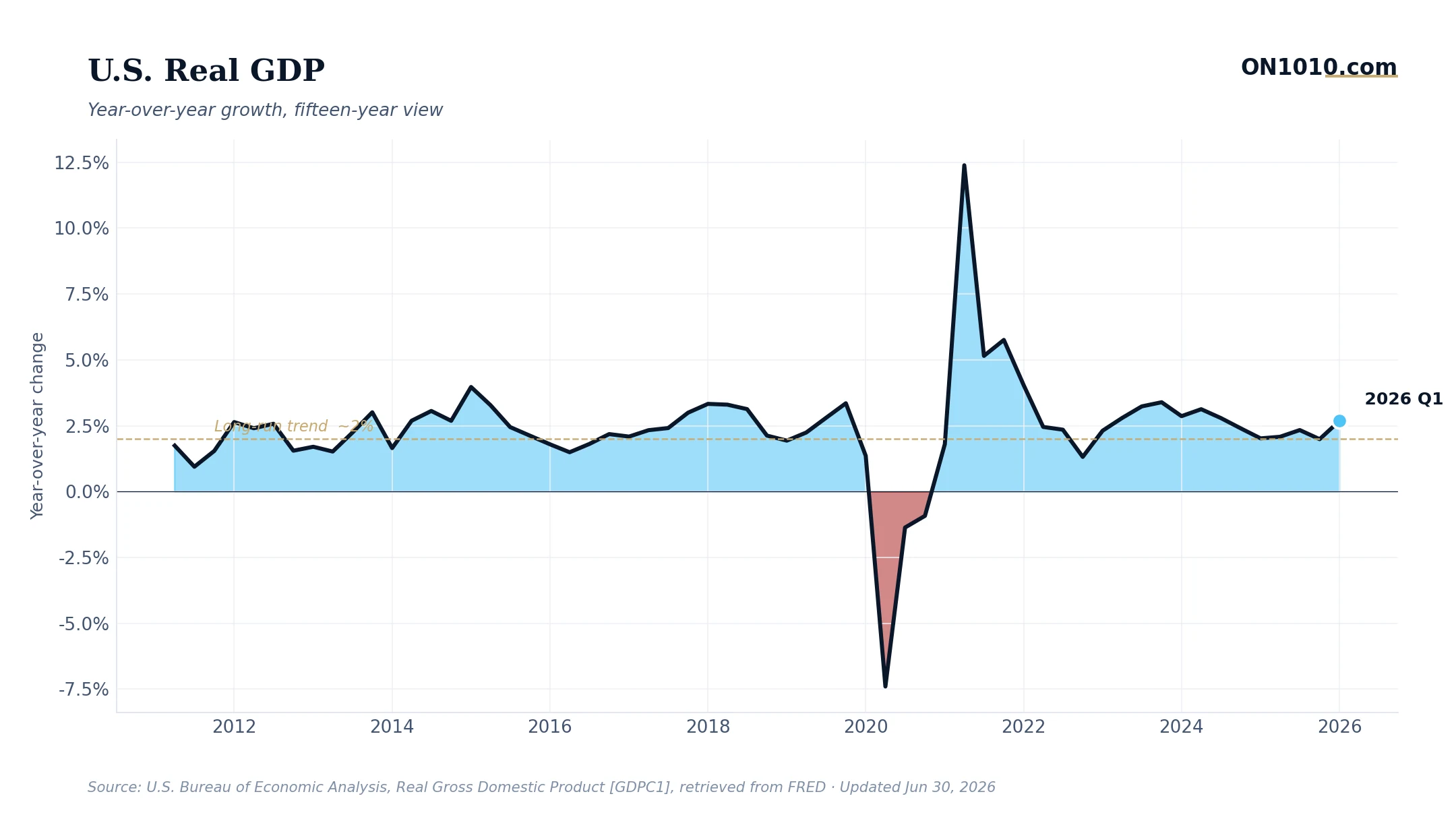

Chinese manufacturing activity grew faster than expected last month, driven by tech export demand. That is the kind of external demand signal that rarely shows up in U.S. headlines until it is already showing up in U.S. earnings.

What moved: The Nasdaq led Monday’s session, rising 2.07% to 25,820, with the S&P 500 adding 1.18% to close at 7,440. The Russell 2000 was essentially flat, up just 0.01%, which is worth noting. When large-cap tech surges and small caps go nowhere, the market is telling you something about confidence in domestic growth versus global tech exposure. The 10-year Treasury yield sits at 4.38%, with the 2-year at 4.07%, leaving a spread of just 28 basis points. Inflation expectations, measured by the 10-year breakeven, remain anchored at 2.22%.

On deck today: No major U.S. data prints this morning, but Tuesday, June 30, 2026 marks the final trading day of the second quarter. End-of-quarter positioning and rebalancing flows can push markets in directions that have nothing to do with fundamentals.

Why it matters: Stronger Chinese factory output means higher demand for the semiconductors, industrial components, and raw materials that U.S. companies supply. If that demand holds, it could support revenue growth at a moment when the domestic picture is still being sorted out.

The deeper read on what this half-year actually meant for the growth cycle lands Sunday in The Long View. It is free, and it is worth the five minutes.

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free