The Yield Curve Just Stopped Moving. That’s More Interesting Than It Sounds.

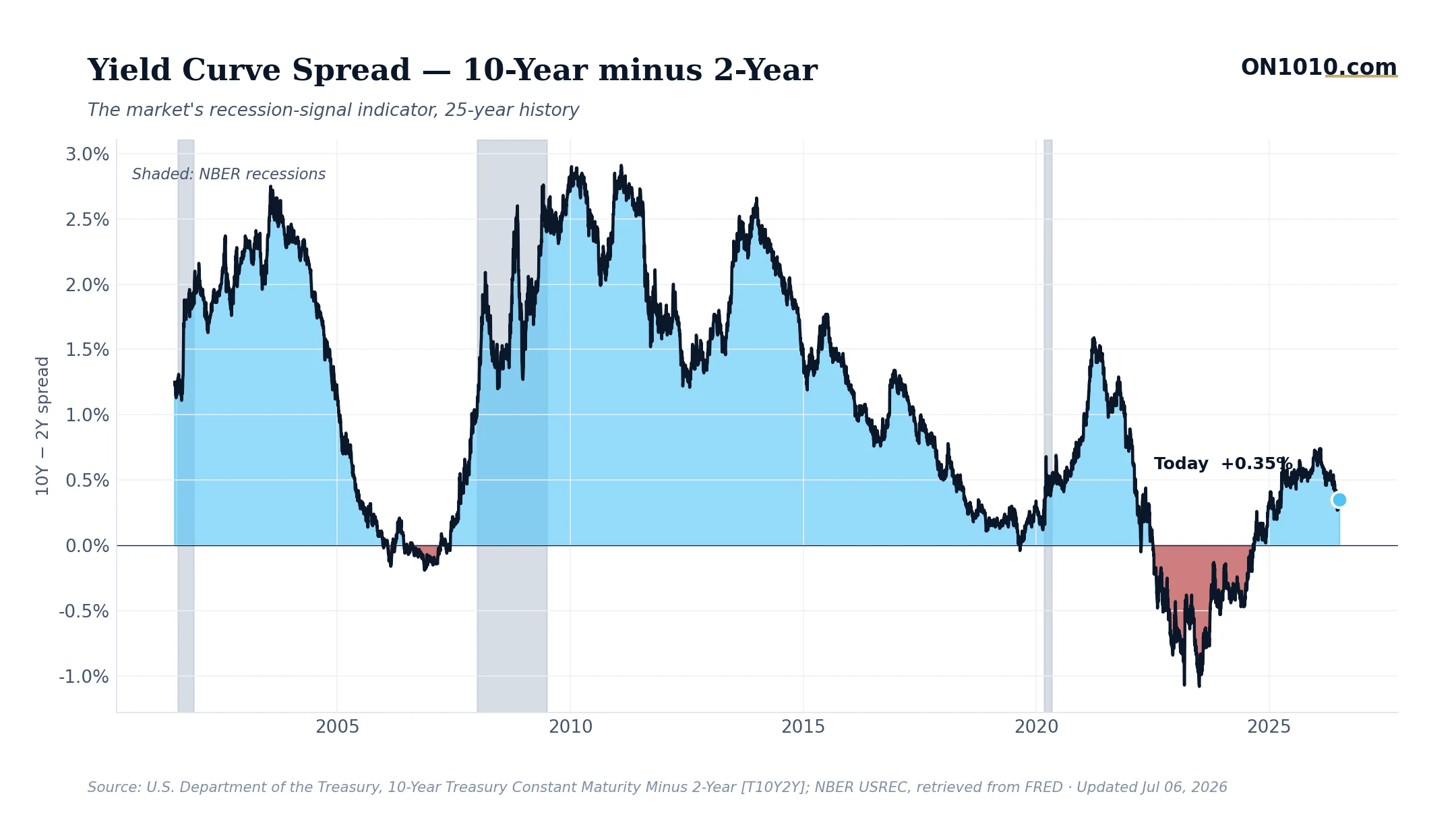

The 10-year minus 2-year Treasury spread has held at 0.35% for two consecutive readings, capping a steady climb from 0.28% just two weeks ago. It doesn’t sound like much, but the direction and the destination both matter here.

Not long ago, this spread sat deep in negative territory, flashing one of history’s most reliable recession warnings. The curve inverted in mid-2022 and stayed there for over two years, longer than almost any prior episode on record. Now it’s back above zero and grinding higher, a process bond market watchers call “re-steepening.” Getting here took time. Holding here is a different test.

Here’s where it gets interesting: the re-steepening is happening at the same time equity markets are sending a mixed message. The broad market is technically in a golden cross formation (50-day above 200-day), which has historically been associated with upward momentum. But money is rotating hard into defensive sectors like health care, utilities, and consumer staples, while technology gets sold. That’s not what a fully confident market looks like.

Historically, the period after a yield curve un-inverts has been uneven. In past cycles, the re-steepening itself sometimes reflected the Fed cutting short-term rates in response to economic weakness, not growth taking off. The key question is always: why is the curve steepening? Is long-term growth optimism pulling long yields up, or is near-term rate cut expectations pulling short yields down? The mechanism matters enormously for what comes next.

In past cycles, business leaders and capital allocators have watched this spread as one input into financing decisions and planning horizons. A steeper curve generally reflects different borrowing economics than a flat or inverted one. As always, the right application to any specific situation belongs with a qualified financial professional.

Bottom Line: The yield curve has re-normalized faster than many expected, but defensive sector rotation is quietly asking a harder question: is this a recovery, or just a pause before the next move down?

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free