The Yield Curve Just Sent Its Most Optimistic Signal in Years. Here’s What to Make of It.

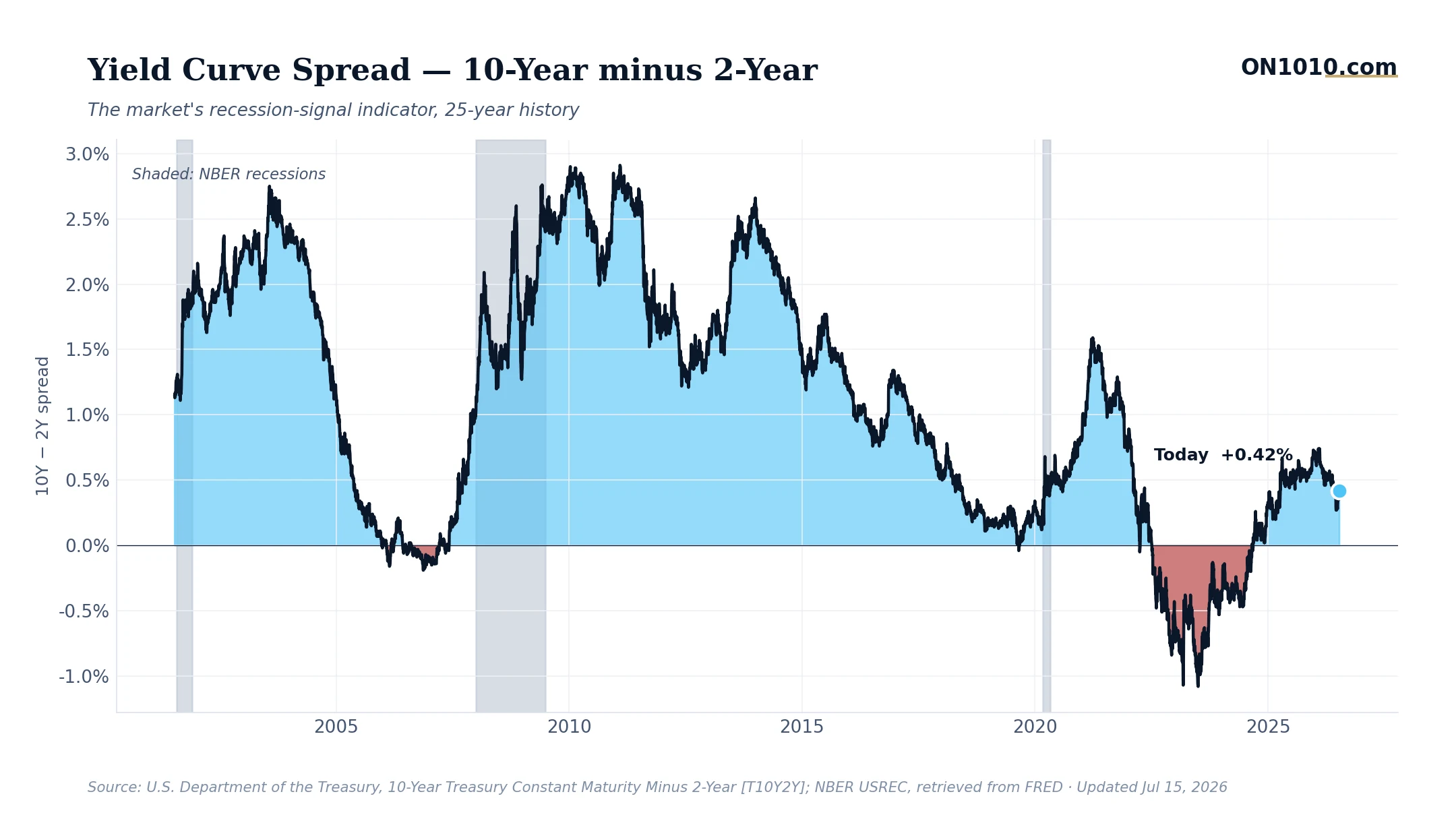

The gap between 10-year and 2-year Treasury yields hit 0.42% on July 15, nudging up from 0.40% the day before and continuing a steady climb that has pushed the spread to its widest positive territory in recent memory. That might sound like a small technical move. It isn’t.

The Bigger Picture

To understand why this matters, you have to remember where we came from. The 10Y-2Y spread spent an extended stretch deep in negative territory, what economists call an inverted yield curve. Historically, that inversion has preceded every U.S. recession since the 1970s, though the timing has varied widely from inversion to recession. The un-inversion, and now the positive drift upward, suggests bond markets are pricing in a more normalized economic outlook. When short-term yields fall relative to long-term yields, it typically means traders expect the Federal Reserve to ease policy, that near-term risk is declining, or that longer-term growth expectations are holding up. In this case, it looks like a combination of all three.

This also fits the broader market picture. Financials and Industrials are leading the equity market right now, both deeply cyclical sectors that tend to outperform when the growth outlook is improving. A steepening yield curve directly helps bank profitability, since banks borrow short and lend long. The spread between those two rates is essentially their profit margin on lending.

Why It Matters

Historically, a positively steepening curve after a prolonged inversion has marked the early phases of a new credit expansion cycle. In past cycles, businesses and capital allocators have watched this signal closely as a sign that financing conditions are becoming more favorable and that the economy may have cleared its highest-risk window. The question worth sitting with: is this steepening driven by falling short rates (a growth concern) or rising long rates (a growth confidence signal)? The answer changes the interpretation considerably.

Bottom Line: The yield curve is healing, and the bond market appears to be endorsing a more constructive economic outlook. Whether that optimism is earned or premature is the question the next few months of data will answer.

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free