Bond Markets Point to Peak Crisis as Tech Rally Tests Fed Resolve

The Opening Bell

Markets are waking up to an odd dynamic: while the Strait of Hormuz remains closed and oil holds near $95, bond yields have stabilized and technology stocks are surging. The question this morning isn’t whether the energy crisis is ending (it isn’t), but whether investors think they’ve seen the worst of it. That shift in sentiment could reshape everything from Fed policy to sector rotation.

Market Snapshot

Fed Funds Target Range: 3.5%-3.75%

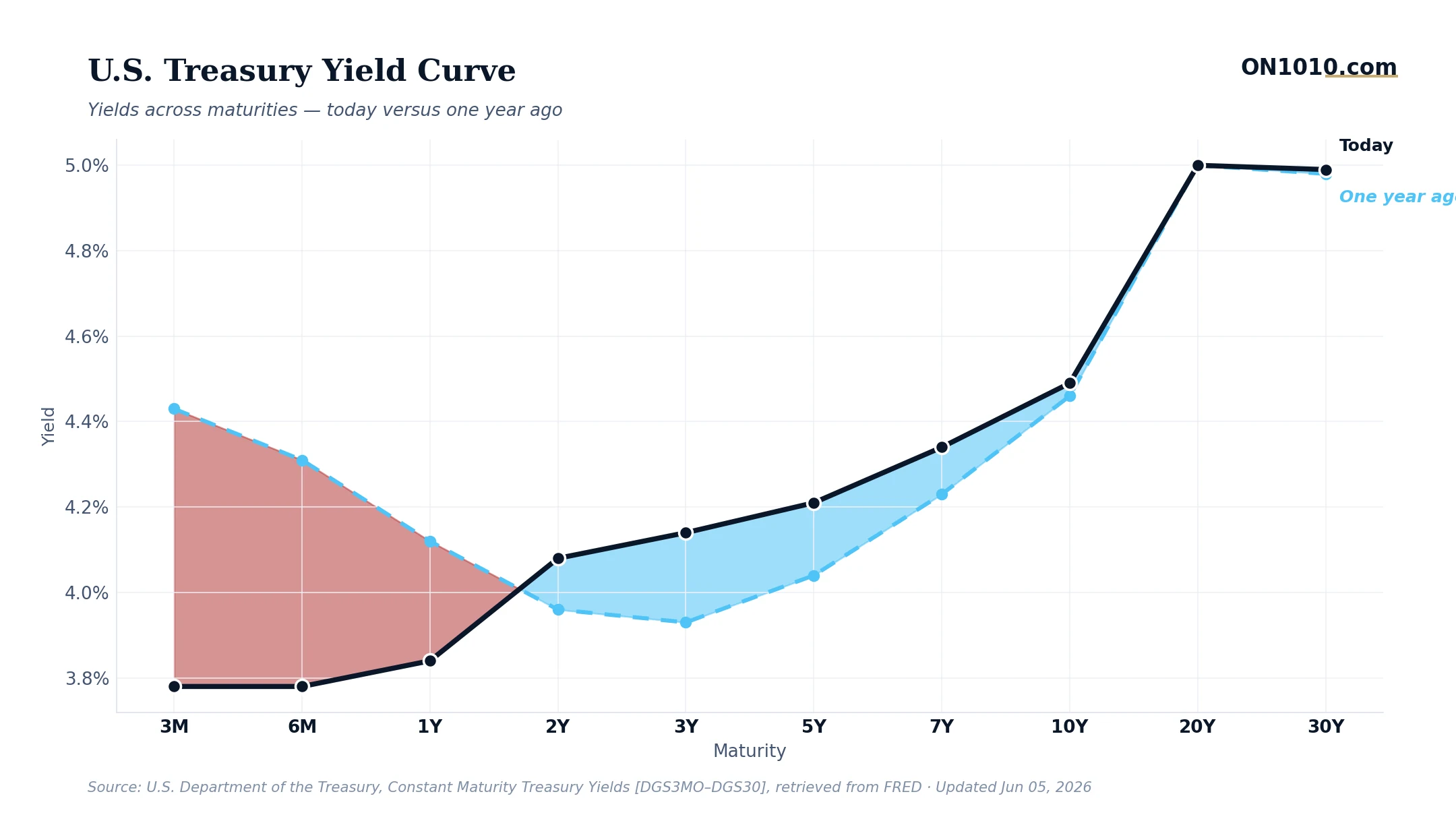

10-Year Treasury: 4.49%

2-Year Treasury: 4.08%

10Y-2Y Spread: 0.42% (normal)

Breakeven Inflation (10Y): 2.36%

The yield curve has quietly normalized over the past month, with the 10Y-2Y spread climbing back into positive territory. More telling: breakeven inflation expectations have actually declined despite oil trading 44% above pre-crisis levels. Bond markets are pricing peak energy shock, not runaway inflation.

What Moved Yesterday

Technology’s 12% outperformance versus the S&P 500 over the past month tells a story about where institutional money thinks this crisis is heading. The sector rotation data shows clear risk-on positioning, with growth stocks leading even as defensive sectors lag. That’s not the pattern you’d expect if investors were bracing for recession or persistent inflation.

The employment picture added nuance. Initial jobless claims jumped to 225,000, the highest reading in over a month and a sharp break from the steady downtrend. But context matters: we’re still well below recessionary levels, and the increase comes as companies navigate energy cost pressures rather than broad demand destruction. The labor market is cooling, not cracking.

Yesterday’s intelligence shuffle headlines reminded investors why uncertainty premium matters. Markets hate policy ambiguity almost as much as they hate actual bad policy. The bond market’s stability suggests investors are pricing through the noise to focus on underlying fundamentals.

Today’s Playbook

Watch the interplay between energy prices and technology momentum. Oil futures are down modestly overnight (WTI at $92.67, down 0.4%), but the real test is whether tech can hold its gains if energy costs spike again. The 50-day moving average at $711.90 for the S&P 500 has become a key support level, with the index now trading well above at $757.09.

Credit markets deserve attention today. Corporate bond spreads have tightened even as some companies report margin pressure from energy costs. If spreads start widening while equity markets stay strong, that divergence could signal trouble ahead. The energy shock creates winners and losers, and bond markets often spot the stress first.

Any Fed commentary will matter more than usual. With breakeven inflation expectations declining despite oil’s surge, policymakers might be gaining confidence that the energy shock won’t trigger broader price pressures. Watch for hints about whether the Fed sees this as a supply shock that will fade or a persistent inflation risk.

The Bigger Picture

The current setup rhymes with 1990-91, when oil spiked during the Gulf War but markets looked through the crisis to economic recovery on the other side. Technology led that recovery too, as investors positioned for productivity growth that would help companies offset higher input costs. The difference now: US energy independence provides a buffer that didn’t exist three decades ago.

China’s resilience during this crisis (90% domestic energy, massive trade surplus) is quietly reshaping global competitive dynamics. US companies competing with Chinese manufacturers face a widening cost disadvantage that could persist even after Hormuz reopens. That structural shift may explain why investors are rotating toward domestic-focused technology plays rather than export-heavy industrials.

Bottom Line: Markets are betting the energy crisis peaks here, with technology leading the way forward. That confidence could prove premature if geopolitical risks escalate, but for now, investors are trading recovery, not recession.

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free