Bond Markets Question Whether Inflation is Really Under Control

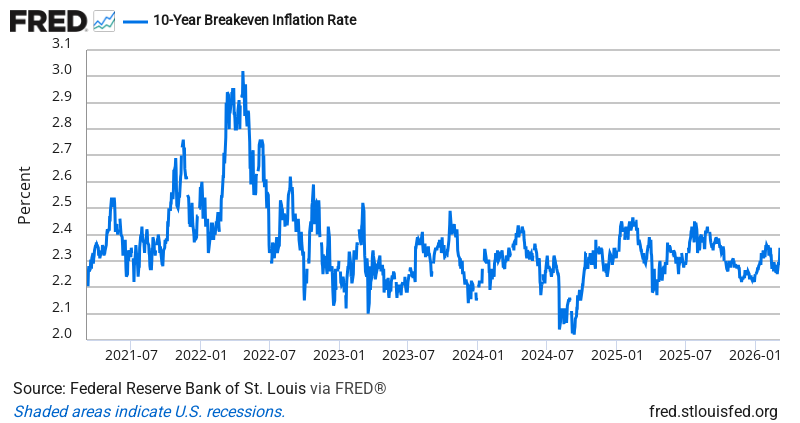

The 10-year breakeven inflation rate jumped to 2.35% yesterday, up 0.04 percentage points from 2.31% the day before. That might sound small, but it represents the biggest single-day move in inflation expectations since early February — and it’s happening just as everyone was getting comfortable with the “inflation is dead” narrative.

Here’s what makes this move interesting: it’s not driven by hot economic data or Fed drama. Instead, it reflects something more subtle but potentially more important — bond traders are starting to price in the reality that 2.35% inflation expectations sit right at the Fed’s target, not below it.

Think about the mechanics here. When breakeven rates rise, it means investors are demanding higher compensation for inflation risk over the next decade. They’re essentially saying: “We’re not confident inflation stays as tame as the recent headlines suggest.” This matters because these same investors are the ones financing everything from corporate expansion to home purchases.

The timing is notable. We’re seeing this uptick in inflation expectations precisely when defensive sectors are crushing offensive ones in the stock market — utilities up 10.3% versus the S&P 500 this month, while financials lag by 5.1%. That’s classic risk-off behavior, suggesting institutional money managers aren’t just worried about growth — they’re positioning for an environment where inflation becomes sticky rather than transitory.

Historically, when breakeven rates climb from these levels, it tends to precede broader questions about monetary policy effectiveness. The last time we saw sustained moves higher from the 2.30% range was in early 2021, right before inflation became the dominant economic story.

In environments like this, professional managers tend to focus on companies with pricing power and real assets that perform well when inflation expectations rise. The question isn’t whether 2.35% breakevens are “high” — it’s whether this marks the beginning of a structural shift higher.

Bottom Line: Bond markets are quietly challenging the “inflation is solved” consensus, and when bond traders start pricing in higher long-term inflation, everything else follows.

Source: Federal Reserve Economic Data (FRED)

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free