Bond Traders Signal Peak Pessimism as China Data Hints at Global Growth Revival

The Opening Bell

Bond traders are quietly unwinding their most crowded bet of the year while fresh data from China suggests the global growth story may be shifting gears. With the Treasury curve steepening to multi-day highs and Chinese manufacturing beating forecasts despite official data weakness, investors are wrestling with a narrative that’s been six months in the making. The question heading into this Monday isn’t whether the energy crisis still matters, but whether other economic forces are finally strong enough to matter more.

Market Snapshot

Fed Funds Target Range: 3.75%

10-Year Treasury: Current data was unavailable at time of writing

2-Year Treasury: Current data was unavailable at time of writing

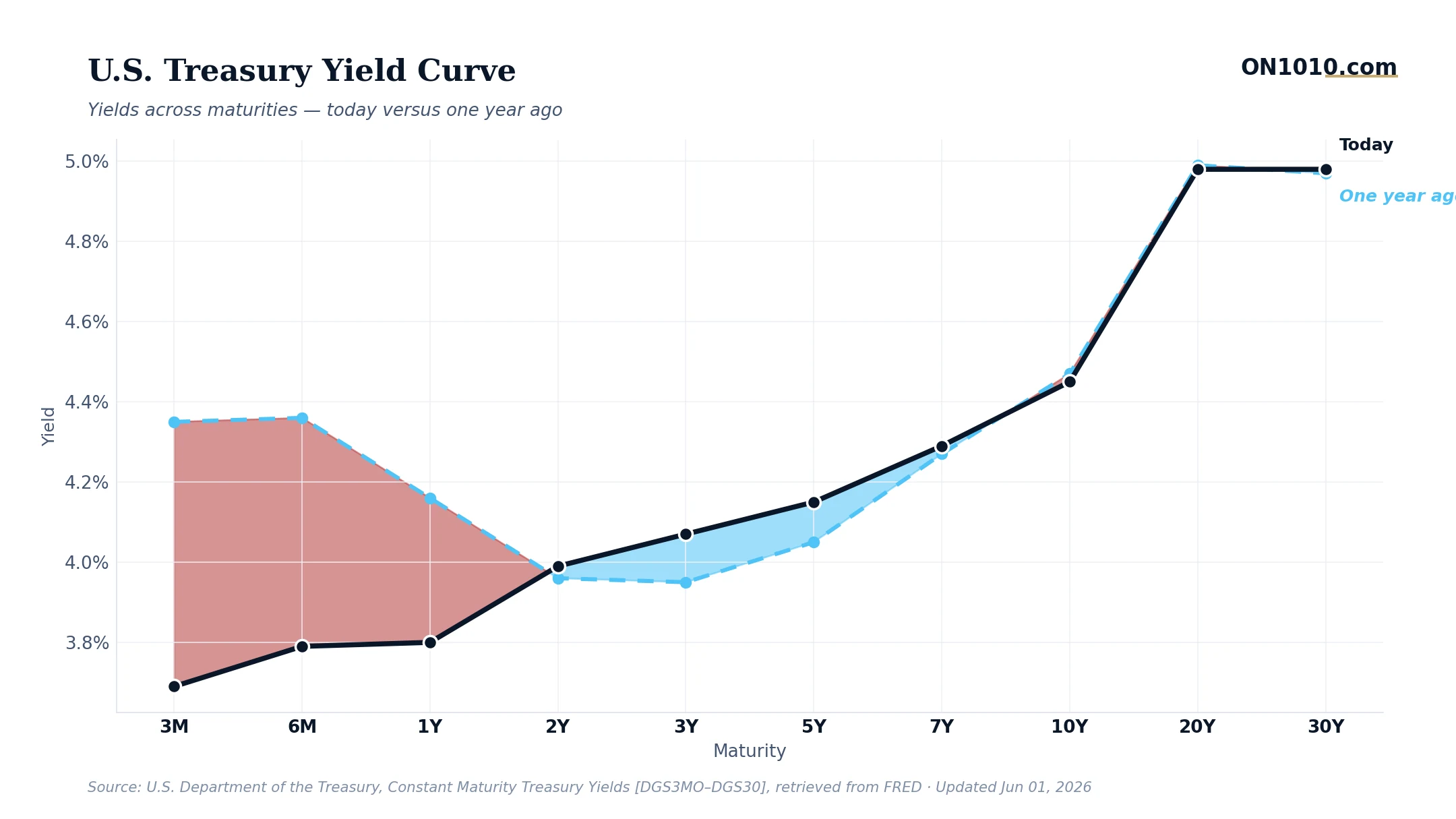

10Y-2Y Spread: 0.47% (normal)

Breakeven Inflation (10Y): Current data was unavailable at time of writing

The 0.47% spread represents the widest normal curve in nearly a week, signaling that traders are backing away from recession bets and pricing in more medium-term growth potential.

What Moved Yesterday

The most telling move wasn’t in headlines but in positioning. Bond traders who spent months betting on curve inversion and recession are quietly covering those trades, steepening the yield curve as they retreat. This technical unwinding reflects something deeper: the market’s growing skepticism that energy shocks automatically trigger recessions in a structurally different economy.

Meanwhile, China’s private PMI data delivered a genuine surprise, beating forecasts even as official manufacturing numbers disappointed. The divergence matters because private surveys often capture smaller manufacturers and service providers who’ve been the real engines of China’s post-reopening growth. When private data outperforms official readings, it typically signals broader-based expansion that government statistics miss.

The combination creates an intriguing setup. Traders are abandoning their recession hedges just as China’s growth engine shows signs of broadening beyond the state-directed infrastructure and export sectors that have driven its 21.8% export surge this year.

Today’s Playbook

Watch how markets digest this positioning shift without major catalysts to guide them. The bond selloff (curve steepening) suggests institutional money is moving away from duration trades and recession hedges. If this continues, expect rotations into cyclical sectors and away from the defensive plays that have dominated since the Hormuz crisis began.

The China data deserves special attention because it challenges a key assumption: that the energy crisis would slow global growth enough to offset inflationary pressures. If China’s domestic economy is actually accelerating while benefiting from cheaper energy costs relative to competitors, that’s a fundamentally different macro picture than markets have been pricing.

Any additional manufacturing data from Asia today will be critical. Japan and South Korea report later this week, and if their numbers show the expected weakness from energy import costs, it reinforces China’s competitive advantage while suggesting global growth is shifting geography rather than simply slowing.

The Bigger Picture

We may be witnessing the early stages of a structural realignment that makes traditional recession playbooks obsolete. The Hormuz closure was supposed to trigger a classic 1970s-style stagflation scenario: slowing growth plus rising prices. Instead, we’re seeing something more nuanced: geographic winners and losers, with growth shifting to energy-advantaged economies rather than disappearing entirely.

This mirrors the 1990s in reverse. Then, technology and globalization created persistent disinflationary pressures that confused central bankers for years. Now, energy geopolitics and supply chain restructuring are creating persistent inflationary pressures alongside continued growth, just in different places. Bond traders seem to be figuring this out ahead of economists.

Bottom Line: The market is quietly admitting that energy shocks don’t automatically mean recession when the global economy has fundamentally restructured around new supply chains and energy sources. If China’s data continues surprising to the upside while developed Asia weakens, expect more traders to abandon their 1970s playbooks.

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free