Gold’s Real Problem Isn’t What Bulls Think

According to CNBC, gold has dropped to its lowest level in six months despite rising inflation fears, with technical weakness and potential rate hikes weighing on prices. Here’s the twist: this isn’t the contradiction it appears to be.

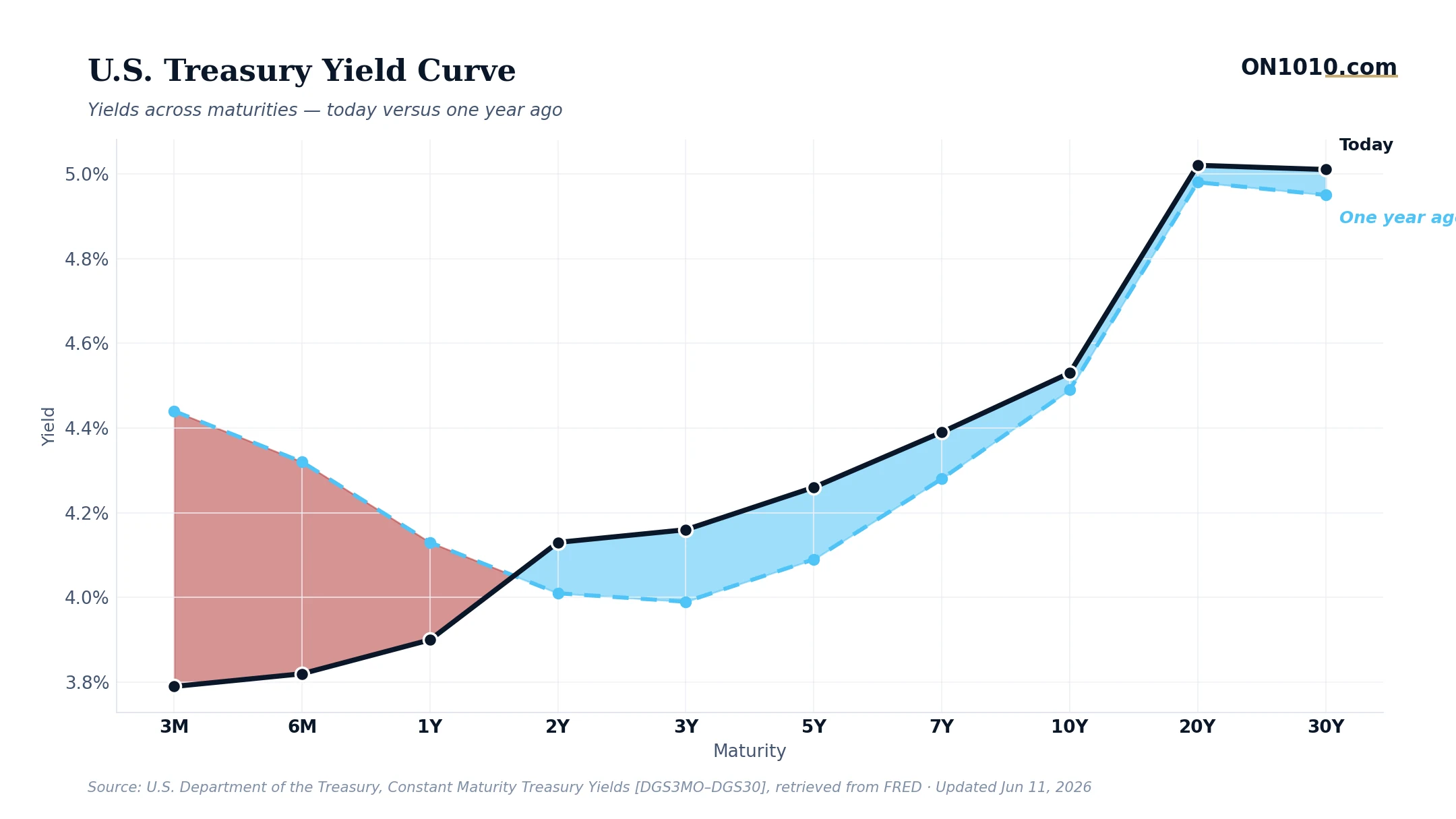

The conventional wisdom says gold should rise with inflation expectations. But that misses the mechanism. Gold thrives when real interest rates are negative, when inflation runs hotter than what bonds pay. With oil at $95 and energy inflation spiking, the Fed has already signaled higher-for-longer is back on the table. If the 10-year yield climbs faster than inflation expectations, real rates turn positive, and gold’s opportunity cost becomes punishing.

There’s also the dollar dynamic. Energy shocks typically strengthen the dollar as global investors flee to safety and oil importers scramble for greenbacks. A stronger dollar makes dollar-denominated gold more expensive for foreign buyers, crushing demand from key markets like India and China. Meanwhile, the equity rotation into defensive sectors suggests institutions are choosing dividend-paying utilities and staples over non-yielding gold as their inflation hedge.

Historically, investors have viewed gold as the ultimate inflation hedge, but the metal actually performs best during stagflation, when growth stalls but inflation persists, leaving central banks paralyzed. Today’s setup looks different: energy-driven inflation hitting an economy that’s still growing, giving the Fed room to tighten if needed.

Bottom Line: Gold is discovering that not all inflation is created equal. When central banks can still fight back, the yellow metal loses its luster.

Read more: CNBC Top News

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free