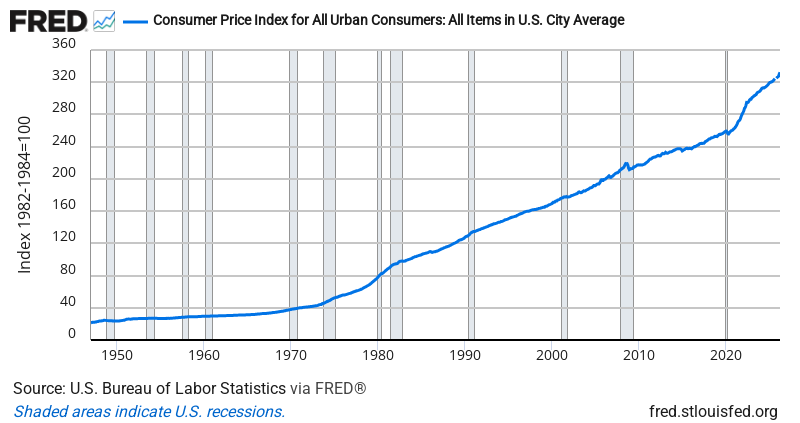

Inflation Accelerates to 3.4% as Price Pressures Broaden

April’s CPI jumped 0.64% month-over-month — the fastest pace since last summer — pushing the annual rate to 3.41% and keeping inflation well above the Fed’s comfort zone.

What’s concerning isn’t just the headline number, but the momentum. We’ve now seen three straight months of accelerating monthly price gains: 0.27% in February, 0.53% in March, and 0.64% in April. That’s the kind of sequential acceleration that makes central bankers nervous. More importantly, it suggests the disinflationary trend that dominated 2023 and early 2024 has stalled — and possibly reversed.

This reading puts us in an awkward spot economically. Inflation is cooling from the 9% peaks of 2022, but it’s also refusing to settle into the Fed’s 2% target range. We’re stuck in what economists call the “last mile” problem — where progress toward price stability becomes increasingly difficult. History suggests this phase can persist longer than markets expect, especially when underlying demand remains strong and labor markets stay tight.

For portfolios, this type of persistent above-target inflation traditionally creates a challenging environment for both stocks and bonds. Many professional investors start considering inflation-protected securities (TIPS) and sectors that can pass through price increases — think energy, utilities, and select commodities. Real assets historically outperform financial assets when inflation proves stickier than expected.

Bottom Line: The Fed’s inflation fight isn’t over, and April’s acceleration suggests we might be settling into a higher-for-longer inflation regime rather than a clean glide path to 2%. The question now is whether this is a temporary bump or the new normal.

Source: Federal Reserve Economic Data (FRED)

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free