Long-Term Inflation Bets Inch Lower Despite Oil Crisis

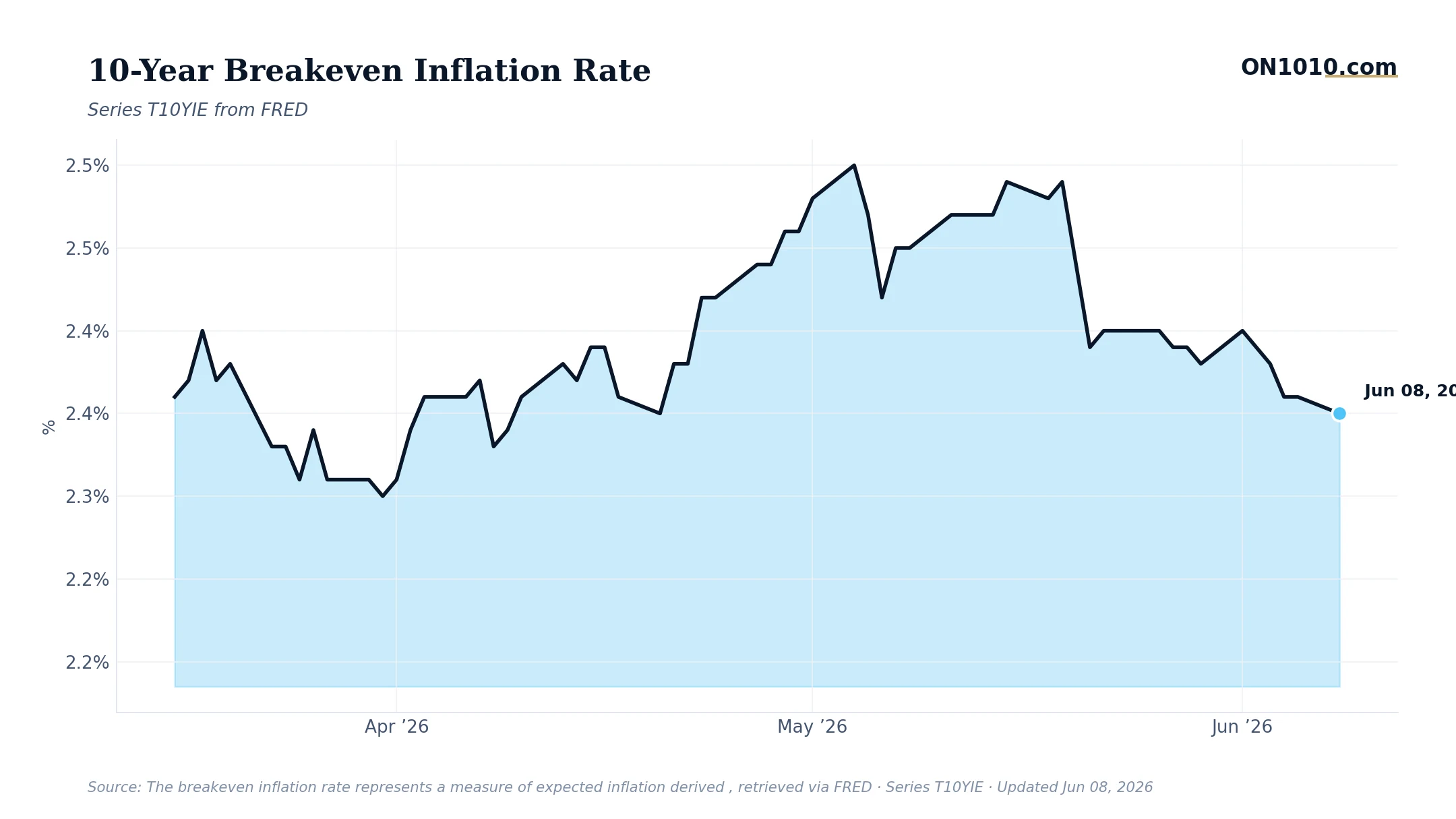

The market’s bet on 10-year inflation dropped to 2.35% Friday, down a tick from 2.36% earlier in the week. That’s a curious move given oil has been trading near $95 since the Strait of Hormuz closure, usually the kind of energy shock that sends long-term inflation expectations higher, not lower.

The decline suggests bond traders are parsing the difference between a temporary oil spike and persistent inflation. Yes, energy prices have jumped 44% since late February. But markets seem convinced this is a supply disruption that will eventually resolve, not the start of a 1970s-style inflationary spiral. The 10-year breakeven has actually been drifting lower all week, from 2.40% on June 1st to today’s 2.35%. That’s bond traders saying: “We’ll take the near-term CPI hit, but we don’t think it changes the underlying disinflationary trend.”

This reading keeps long-term expectations well within the Fed’s comfort zone, even as short-term inflation risks have pushed rate cuts off the table. Historically, breakeven rates above 3% have triggered more aggressive Fed hawkishness. Below 2%, and deflation fears creep in. The current 2.35% level sits in the sweet spot, acknowledging energy-driven price pressures without signaling a fundamental shift in inflation dynamics. It’s also worth noting that in past energy crises, breakeven rates often stayed elevated longer than the underlying commodity shock lasted.

In past cycles, this type of restrained long-term inflation expectation during an active energy crisis has meant investors expected either quick resolution or economic slowdown to offset price pressures. The question for business leaders watching their input costs: are you planning for a temporary margin squeeze that reverses when the Strait reopens, or a longer period of higher energy prices that requires more structural adjustments?

Bottom Line: The bond market is betting this oil shock burns hot but brief. Whether that confidence proves right depends more on geopolitics than economics, and geopolitics rarely cooperate with market timelines.

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free