The Fed Is on Pause. Here’s What That Silence Is Saying.

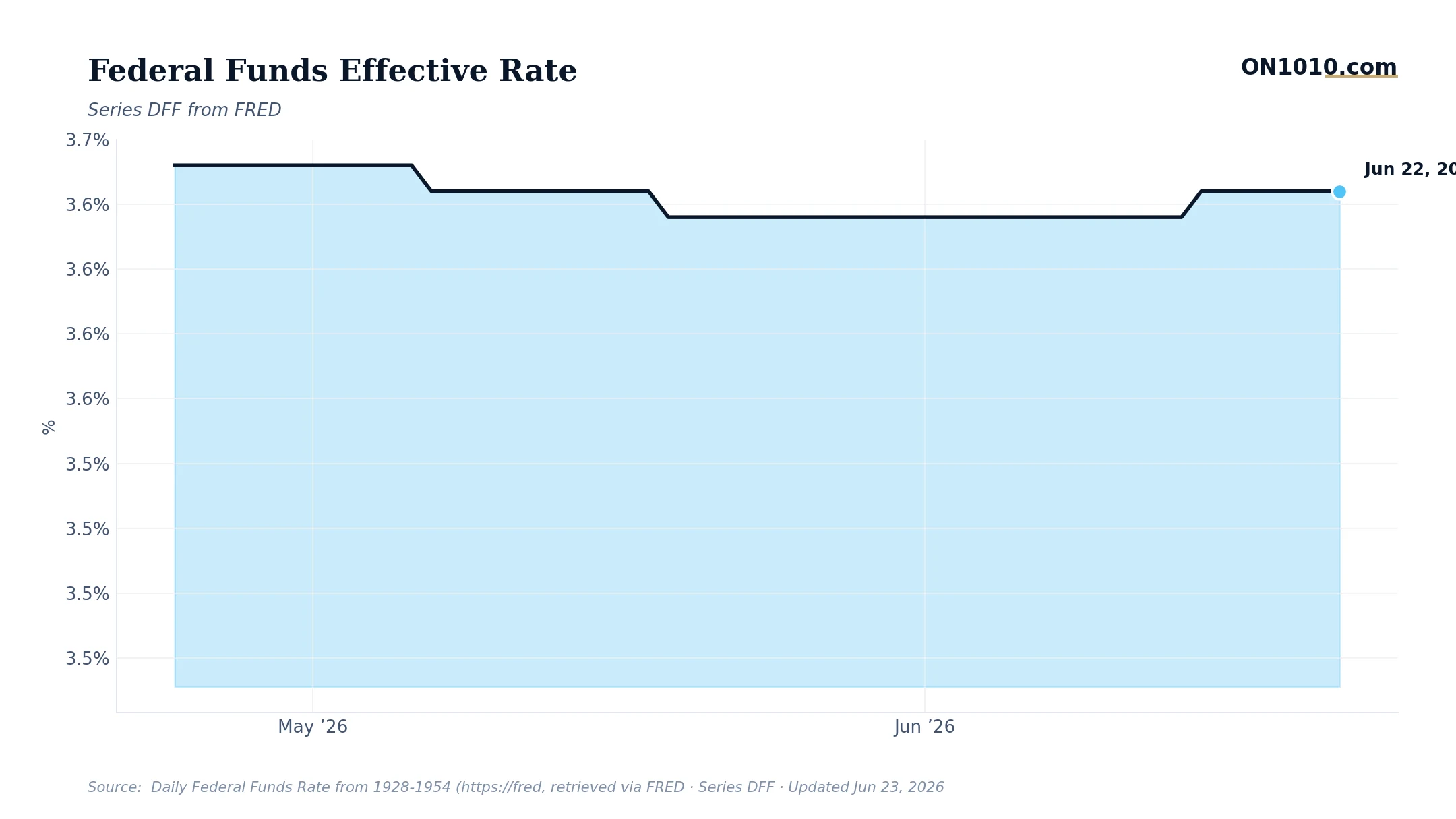

The effective federal funds rate has sat at 3.63% for six straight days, and that stillness is the story. The Fed isn’t just holding rates, it’s holding its breath.

When the Strait of Hormuz closed in late February following U.S.-Israel strikes on Iran, the calculus for rate cuts changed overnight. Before the energy shock, CPI and PCE were settling near 2.5% annually, and markets were pricing in a gradual easing path. Now, with oil having already spiked substantially from pre-crisis levels, every sustained 10% premium in crude adds roughly 0.6% to CPI. Monthly inflation prints could start registering with a 1-handle. In that environment, cutting rates would be like pouring fuel on a fire.

The effective funds rate is the one monetary policy signal that can’t be spun or revised. When it stops moving, the Fed has made a decision, and right now that decision is: we wait.

Historically, this kind of abrupt pause in an easing cycle, especially one triggered by an external supply shock rather than domestic demand strength, has created a tricky environment. Rate cuts that markets had priced in get repriced away, which pushes up longer-dated yields and tightens financial conditions even without the Fed doing anything new. In past cycles, businesses watching this dynamic have paid close attention to whether the pause is temporary (shock fades, cuts resume) or whether it signals a longer regime shift toward higher-for-longer. The market’s current VIX of 19.82, slightly above its 20-day average, suggests some unease without full alarm.

For now, the 3.63% rate is a placeholder, not a destination. The question isn’t what the Fed has done. It’s how long the energy crisis forces their hand to stay exactly here.

Bottom Line: A rate that doesn’t move still tells a story. The Fed is frozen between an inflation shock it didn’t create and an economy that hasn’t broken yet. Watch the monthly CPI prints closely. They will determine whether 3.63% is a ceiling, a floor, or a turning point.

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free