The Fed’s Inflation Problem Just Got Smaller. Here’s What the Market Already Knew.

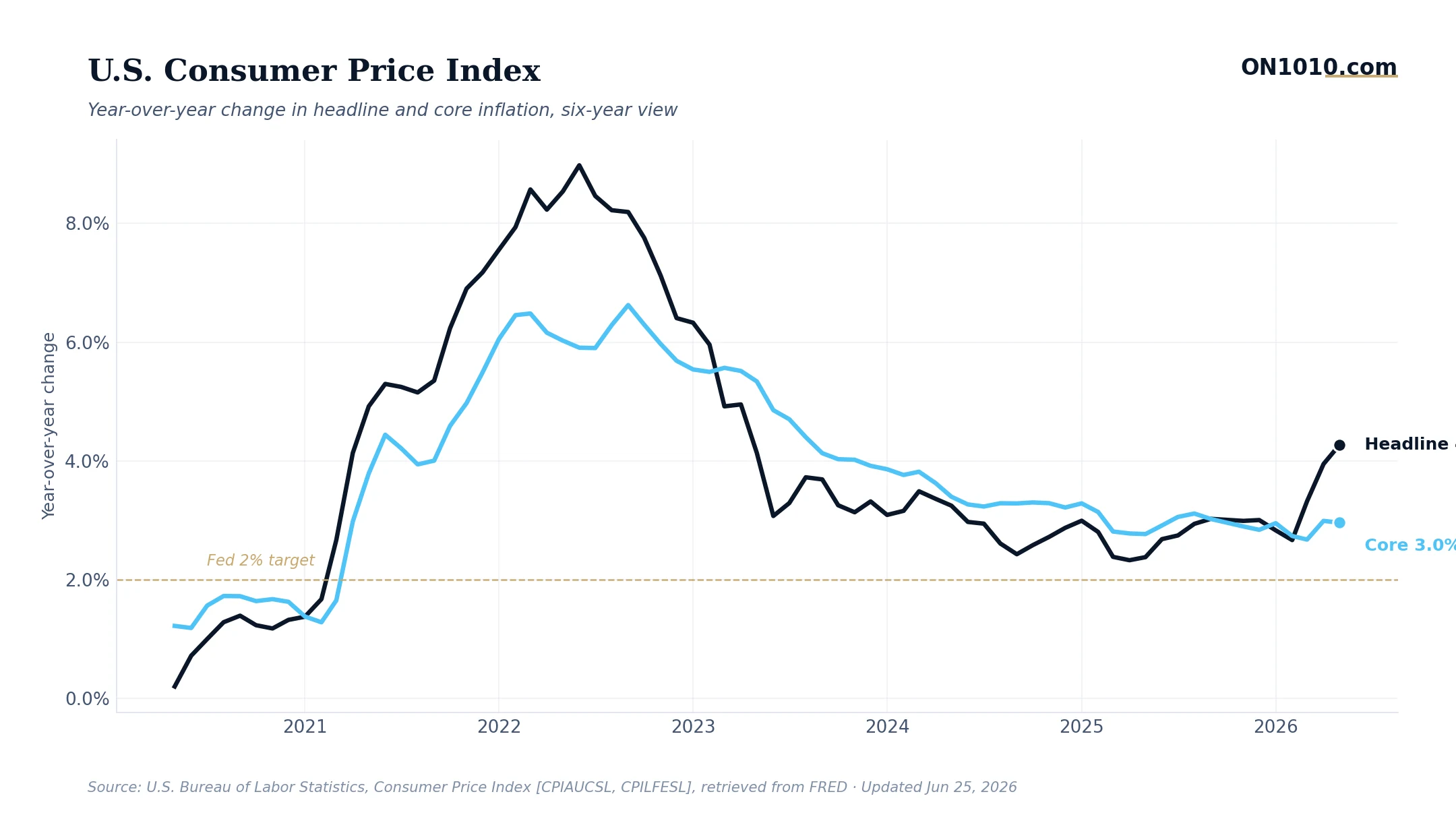

According to CNBC, the Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, showed core inflation running at 3.4% annually in May 2026, the highest reading since October 2023, but meaningfully below the 4.1% that economists had expected. That gap between forecast and reality is the story.

A miss that big in the favorable direction is not a rounding error. When the consensus expects 4.1% and gets 3.4%, something in the inflation machinery is moving faster than analysts modeled. The most likely culprits are easing goods prices, a trend driven by stabilizing supply chains and softer consumer demand in discretionary categories, and a labor market that, while still healthy, is no longer throwing fuel on the wage-price spiral the way it was in 2022 and 2023. Core PCE, now sitting at an index level of 131.527 (FRED, May 2026), is still above the Fed’s 2% target, but the direction and the surprise both point the same way.

This matters because the Fed has been explicit: it is watching PCE more than CPI, and it is watching the trend more than any single print. A reading that comes in 70 basis points below expectations shifts the probability distribution around rate cuts without requiring the Fed to say a word. Historically, when core PCE has surprised to the downside after a period of elevated readings, fixed income markets have moved quickly to reprice the path of the federal funds rate. The equity market’s current positioning, with industrials and financials leading on the year and the S&P 500 trading above both its 50-day and 200-day moving averages, suggests that capital has already been making a bet that the inflation story was improving. Today’s data offers some confirmation.

The question worth sitting with is whether one better-than-expected print is the start of a durable disinflation trend, or a single soft month before tariff-driven goods prices push the index back up.

Bottom Line: The headline was “inflation hit a high.” The real story is that it came in far below what anyone feared, and that distinction is worth more than the number itself.

Read more: CNBC Economy

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free