The Yield Curve Is Positive Again. Here’s Why That’s Worth Watching.

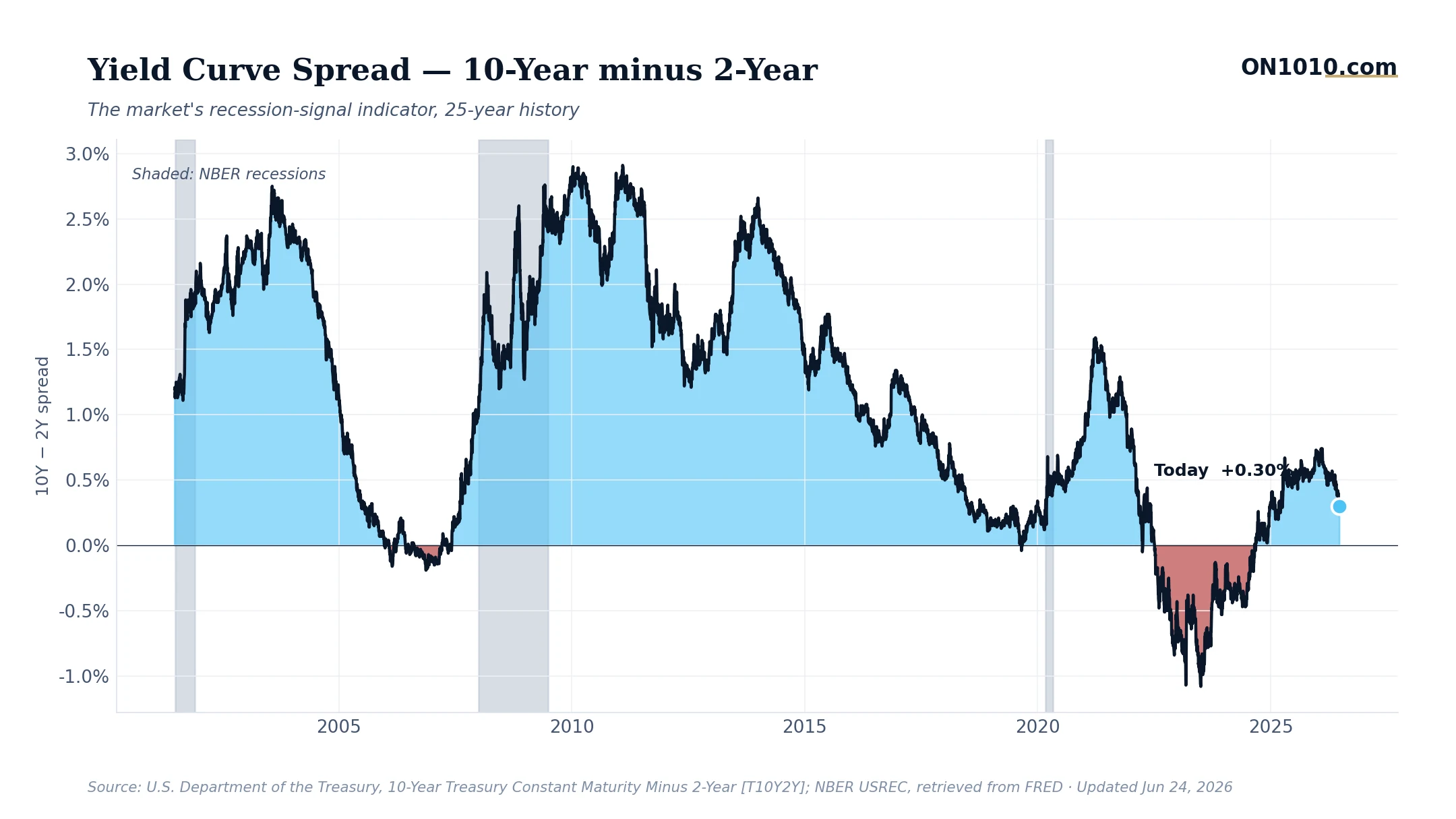

The 10-year/2-year Treasury spread sits at 0.30% as of June 24, a small dip from 0.34% the day before, but still firmly in positive territory. That might not sound like a headline. But given where this spread has been over the past two years, it matters more than the decimal place suggests.

For most of 2023 and into 2024, this spread was deeply inverted, meaning short-term rates were higher than long-term rates, which has historically preceded recessions. The fact that the curve has now been positive for several months, and holding in a range of 0.27% to 0.38% over the past week, signals something the data has been quietly building toward: the bond market is no longer pricing in an imminent economic collapse.

This lines up with what equity markets are telling us. The S&P 500 is trading above both its 50-day and 200-day moving averages in a classic “golden cross” pattern. Industrials and Financials are outperforming the broader index by 5% or more. Those are sectors that tend to do well when the economy is growing and credit conditions are opening up, not tightening.

Historically, the transition from inversion back to a positively sloped curve has been a two-sided story. In past cycles, it has sometimes meant the storm passed, and in others it marked the start of a slowdown that arrived anyway but on a delay. The direction and speed of the re-steepening have mattered as much as the sign itself. Business leaders watching this indicator have used it as a signal for how accessible long-term capital is becoming relative to short-term borrowing costs.

Bottom Line: The curve is positive, the equity trend is intact, and institutional money is leaning toward growth sectors. The question worth sitting with: is this a true all-clear, or a curve that’s still finding its footing after one of the longest inversions on record?

Source: Federal Reserve Economic Data (FRED)

ON1010 Research is an independent publisher of economic education and is not a registered investment adviser, broker-dealer, or investment company. This content is for educational and informational purposes only and is not investment advice or a recommendation to buy, sell, or hold any security. Published under the publisher exemption recognized by Section 202(a)(11)(D) of the Investment Advisers Act of 1940 (Lowe v. SEC). Always consult a qualified financial professional before making any financial decision.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free