The Yield Curve Is Quietly Going the Wrong Direction

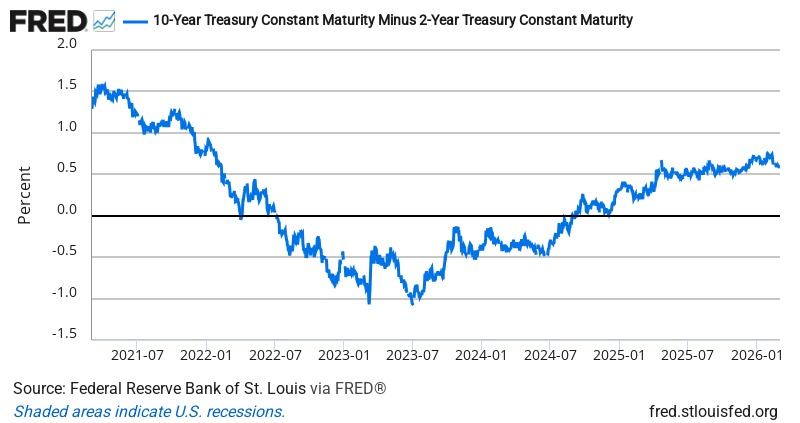

The yield curve spread between 10-year and 2-year Treasuries fell to 0.58% last week, down from 0.59% the week before. That’s the fifth consecutive day of narrowing, bringing the spread back to levels not seen since late January.

Here’s what makes this interesting: the curve has been steepening steadily since November, when it hit a post-inversion low of around 0.20%. That steepening was supposed to signal the all-clear on recession risk. Now it’s quietly reversing course, and the timing couldn’t be more curious.

The conventional wisdom says a steepening curve means economic growth ahead, while narrowing suggests trouble brewing. But that framework misses something crucial about today’s bond market. When the curve steepens because long rates rise faster than short rates, that’s different from steepening because short rates fall faster than long rates. The first suggests growth expectations. The second suggests the Fed cutting rates into weakness.

Right now, we’re seeing something else entirely: both ends moving lower, but short rates falling faster. The 2-year yield has dropped about 15 basis points over the past two weeks, while the 10-year has only fallen 10 basis points. That pattern typically emerges when bond traders start pricing in Fed cuts, but they’re not panicking about growth yet.

This creates a puzzle for investors watching recession signals. The curve spent most of 2023 deeply inverted, flashing red warning lights that never quite materialized into economic collapse. Now that it’s positive again, a narrowing spread doesn’t carry the same recession signal it would in normal times. We’re in uncharted territory where the traditional playbook doesn’t quite apply.

Historically, professional managers have used yield curve moves as a leading indicator for sector rotation. When spreads narrow after being inverted, defensive sectors tend to outperform. When spreads widen from positive territory, cyclicals usually lead. The current narrowing suggests bond traders are getting cautious about something, even if they haven’t figured out exactly what yet.

Bottom Line: The yield curve is moving in the wrong direction for growth bulls, but it’s not screaming recession either. In a post-inversion world, maybe a slightly narrowing positive curve is just the new normal?

Source: Federal Reserve Economic Data (FRED)

ON1010.com provides economic education for investors. Nothing here is investment advice. Always consult a qualified financial advisor before making investment decisions.

Free Research

The economy moves fast. We make sure you move faster.

Economic data, policy shifts, and market signals — delivered to your inbox.

Subscribe Free